Video KYC: How Remote Video Verification Works & Where It's Required

Opening a bank account used to mean a branch visit, a queue, and a folder of photocopies. Video KYC replaces all of that with a short video call: a customer connects from their phone, shows their ID to camera, and is verified in minutes. It is one of the few remote-onboarding methods that regulators in some countries accept as a full, in-person-equivalent identity check.

This guide explains what video KYC is, how the process works step by step, how it differs from eKYC and a plain selfie check, where it is legally required or recognized around the world, and whether it is safe.

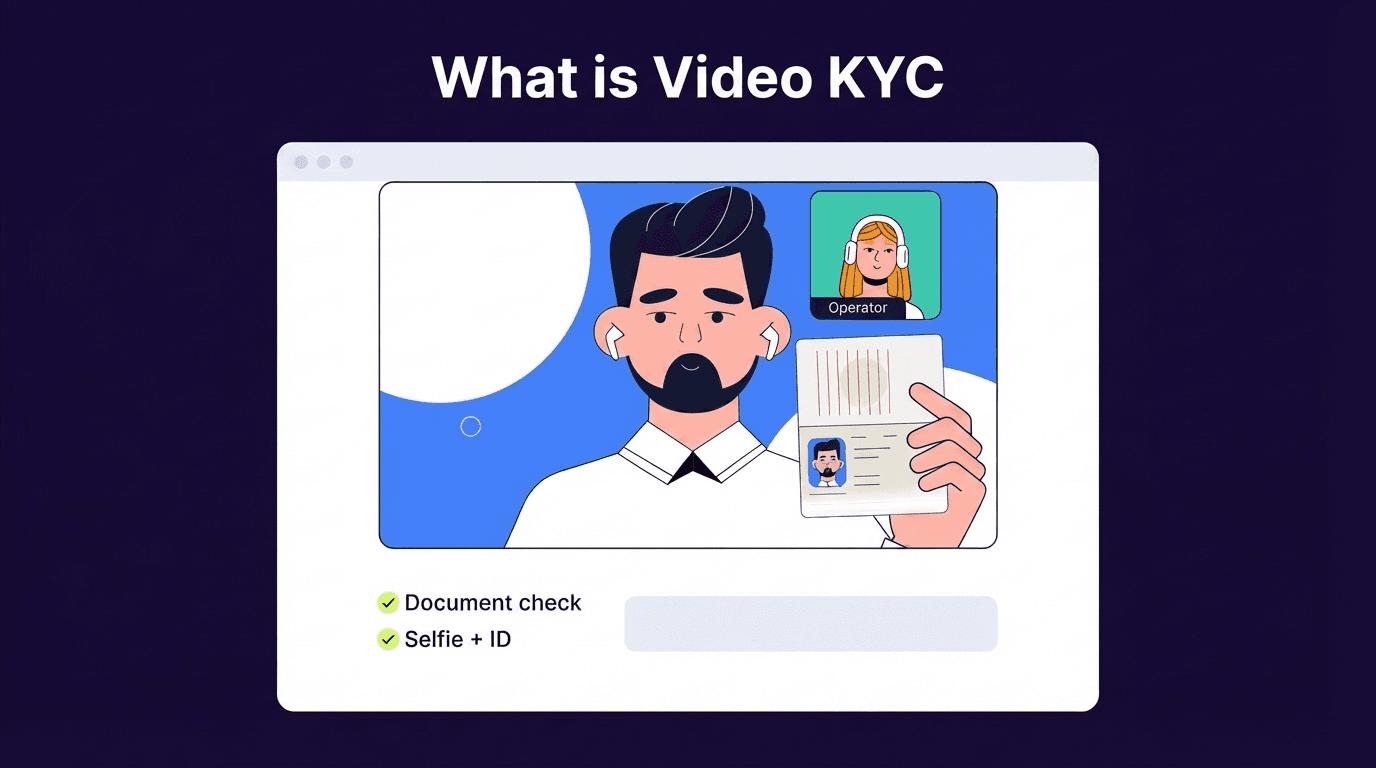

What Is Video KYC?

Video KYC is a method of verifying a customer's identity remotely during a live video session, combining document capture, face matching, and liveness detection with an agent-led or AI-guided interview.

It lets a regulated business complete a full Know Your Customer check without the customer ever visiting a branch. In India, where it is most established, it is known formally as V-CIP, the Video-based Customer Identification Process, introduced by the Reserve Bank of India in 2020. Elsewhere it is often called video identification or video-based verification.

How Does Video KYC Work?

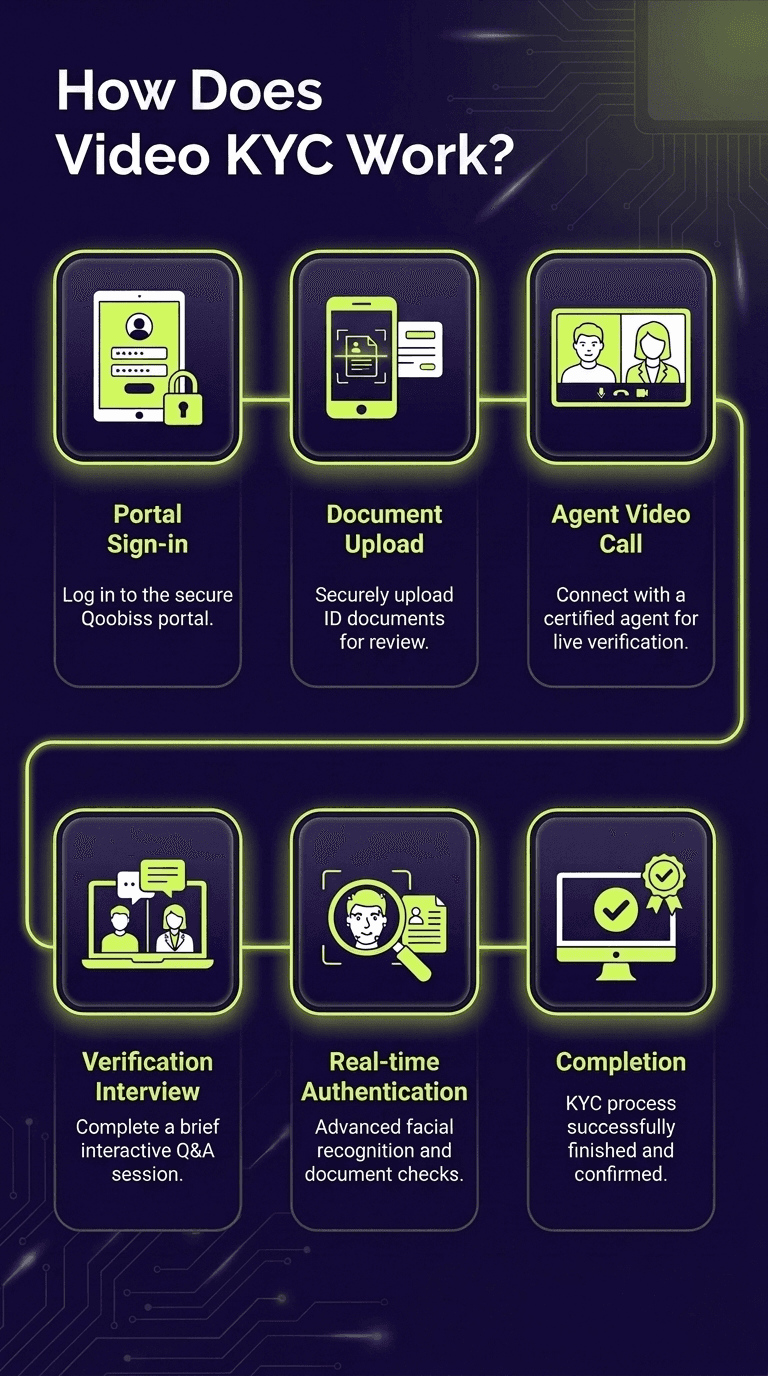

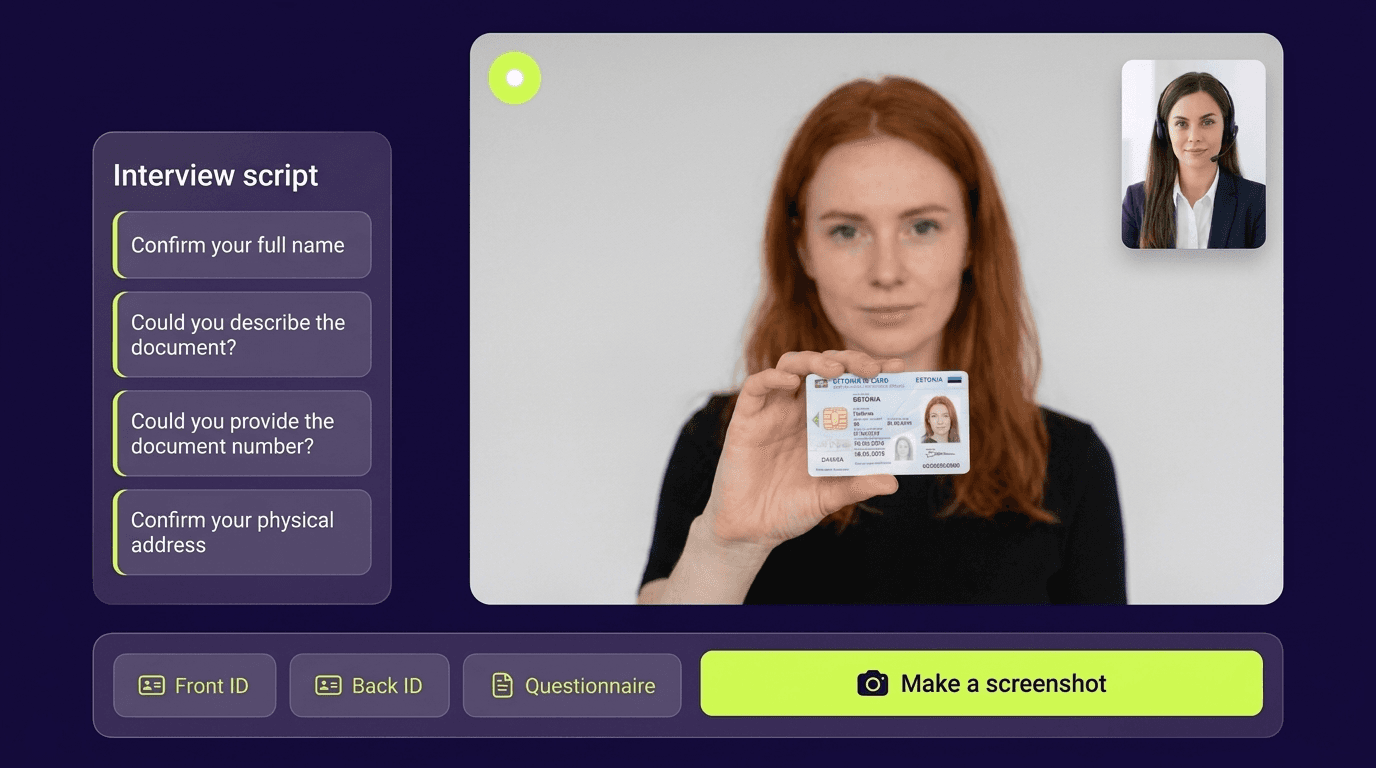

Behind what feels like a short video call is a sequence of checks that together stand in for the trust a face-to-face meeting used to provide. Each step verifies a different thing: that the document is real, that the person matches it, that they are genuinely present, and that the whole session can be evidenced later. A typical flow runs as follows, and most sessions finish in three to five minutes.

Initiate the session. The customer begins onboarding online and opens a secure, single-use video link, usually sent by SMS or email and valid for a limited time. Most flows run in a mobile browser with no app to download, which keeps drop-off low. Behind the scenes the session is tied to that specific applicant so the recording can be matched to their file.

Capture identity data and documents. The customer enters basic details and presents an identity document to the camera, such as a passport, national ID, or in India a PAN card. OCR reads the fields, NFC chip reading can pull the same data cryptographically from an e-passport, and automated checks look for signs of tampering, altered fonts, or a document that is a photo of a screen rather than the real thing.

Connect and verify live. The customer joins a live session with a trained agent, or an AI-guided flow in automated models. The reviewer confirms the physical document on camera, checks it against the extracted data, and captures a live photograph of the customer. In agent-led models this is also where a human forms a first judgement about whether anything looks staged or coached.

Match the face and confirm liveness. The customer's face is matched against the photo on the document to confirm they are the same person. At the same time, liveness detection confirms a real, physically present human rather than a photo, a replayed video, a mask, or an injected deepfake. Stronger systems combine passive analysis with active prompts, such as asking the customer to turn their head or follow an on-screen movement.

Geotag and record consent. The customer's location and explicit consent to be recorded are captured. Location matters because some regimes require the customer to be physically inside the jurisdiction; India's rules, for example, require the person to be in India during the session. Consent and the terms shown are logged as part of the record.

Ask verification questions. The agent, or the guided flow, asks a few unscripted or randomized questions. This confirms the interaction is genuinely live rather than a pre-recorded video, and gives the reviewer a chance to spot a customer who is being coached or coerced off-camera. Randomizing the questions is what stops fraudsters from preparing a scripted response in advance.

Decide, and store the evidence. The system combines the document, face, liveness, and behavioral signals into a single risk decision, either approving the customer, routing them to manual review, or declining. The encrypted video recording, still images, and a structured audit log are retained, often for five to ten years to meet FATF and local record-keeping rules, so the check can be reproduced for a regulator or auditor.

Agent-led, automated, or hybrid

Video KYC comes in three flavors:

1. Agent-led sessions use a live human reviewer, which many regulators require.

Automated (assisted) flows use AI to guide and verify without a live agent, and

Hybrid models let AI handle document, face, and liveness checks while an agent oversees higher-risk cases. Which is permitted depends on the jurisdiction.

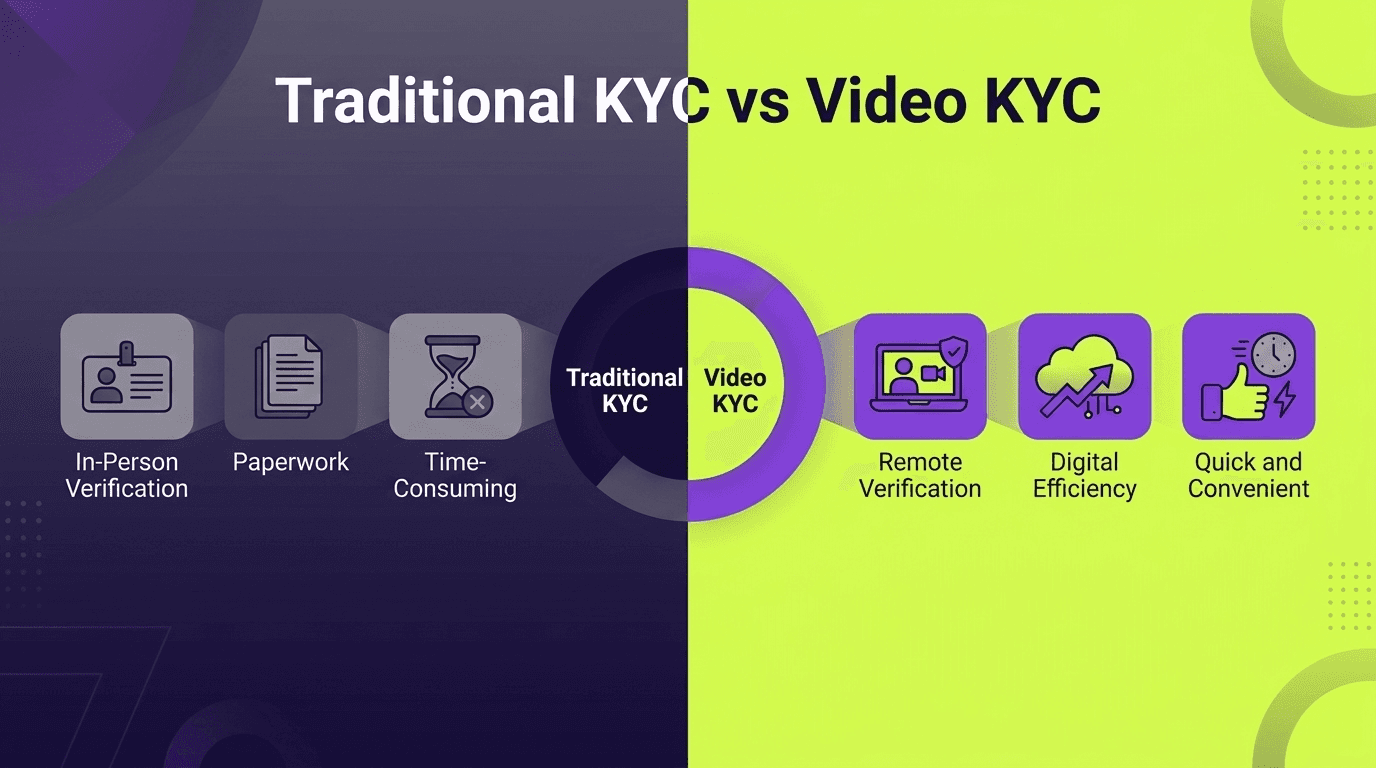

Video KYC vs eKYC vs Traditional KYC

These three terms are often used loosely, but they describe different things, and mixing them up leads to the wrong compliance decisions. Traditional KYC is the in-person original. eKYC is the fully digital, automated version. Video KYC sits in between: fully remote, but with a live, real-time human or guided element that some regulators treat as equivalent to meeting in person.

In practice, eKYC captures and checks data automatically, while video KYC adds a live verification layer on top. The two are not rivals: many onboarding journeys start with eKYC (scan an ID, take a selfie) and escalate to a video session only for higher-risk customers or where local rules demand a live check. Think of eKYC as the fast default and video KYC as the higher-assurance option.

It is also important not to confuse video KYC with a simple selfie or liveness check. A passive selfie confirms that a real, live person is present, and it is one component of the process.

Video KYC is the full session around it: a verified document, a face match, a live interaction with unscripted questions, geotagging and consent, and a recorded, auditable trail. That combination is what lets regulators in some countries accept it as a full identity verification rather than a single signal.

Method | How identity is verified | Presence |

|---|---|---|

Traditional KYC | Physical documents checked by staff, often in a branch | In person |

eKYC | Fully digital: document scan, selfie, liveness, database checks, usually automated | Remote, asynchronous |

Video KYC | Live video session with document, face match, liveness, and an interview | Remote, real-time |

In practice, eKYC captures and checks data automatically, while video KYC adds a live, real-time verification layer that some regulators treat as equivalent to meeting in person. It is also more than a selfie check: a passive selfie confirms liveness, whereas video KYC is a full session with a document, an interview, and an audit trail.

Where Is Video KYC Required or Recognized?

Whether video KYC is mandatory, optional, or simply accepted depends entirely on the country. The picture below reflects well-established positions; because AML rules evolve, confirm current specifics with each regulator.

Jurisdiction | Regulator / framework | Status of video identification |

|---|---|---|

India | RBI, via V-CIP (2020 KYC Master Direction amendment) | Formally defined and widely used for full remote KYC |

Germany | BaFin, under the Money Laundering Act (GwG) | Video identification (VideoIdent) explicitly permitted |

Spain | SEPBLAC | Video identification recognized for remote onboarding |

European Union | AMLR/AMLA and eIDAS 2.0 direction; EBA remote-onboarding guidance | Remote and video-based CDD supported, with liveness expected |

United Kingdom | FCA, risk-based; digital identity trust framework | Accepted as part of risk-based electronic verification |

United States | FinCEN CDD Rule (BSA) | Non-documentary and remote methods permitted; no single video mandate |

Gulf (UAE, KSA) | Central-bank circulars | Video-based onboarding permitted under conditions |

A few patterns are worth drawing out of that table. India is the clearest case: the Reserve Bank of India defined video KYC as a formal process (V-CIP) with a detailed rulebook, which is why the method is so widely used there and why most online guides to video KYC are India-focused.

Germany pioneered it in Europe, where BaFin has long permitted video identification (often called VideoIdent) as a recognized way to meet obligations under the Money Laundering Act, and Spain's SEPBLAC followed with its own recognized video-identification standards.

The broader European Union is moving toward harmonized remote onboarding: the incoming AML Regulation and the new AML Authority (AMLA), together with the direction set by eIDAS 2.0 and the EU Digital Identity Wallet, point to remote and video-based customer due diligence being supported across member states, with strong liveness and anti-fraud measures expected.

The United States takes a different approach: rather than mandating a specific method, the FinCEN Customer Identification Program rules let firms use documentary and non-documentary verification, so video is permitted as one option within a risk-based program rather than required.

The practical takeaway for a business operating across borders is that there is no single global standard. A video KYC flow that satisfies India's V-CIP will not automatically meet Germany's or the EU's expectations, and vice versa. Firms usually build a configurable process that can add or drop steps (geotagging, a live agent, specific document types) to match each market it operates in.

For the EU trajectory specifically, see our guide to eIDAS 2.0 and the EU Digital Identity Wallet.

India's V-CIP requirements

Because India's rules are the most detailed, they are a useful reference for what a compliant video KYC looks like. RBI's V-CIP generally requires:

A live photograph of the customer captured during the session

Verification of the customer's PAN and Aadhaar-based or officially valid documents

Geotagging to confirm the customer is located in India

Random or unscripted questions to confirm the interaction is live and genuine

A trained official conducting the session in real time

End-to-end encryption and a stored, auditable recording

What You Need for Video KYC

One of the advantages of video KYC is how little it asks of the customer: no printer, no scanner, and no trip to a branch.

That said, a smooth session depends on being properly set up before the call starts, because most failed or repeated sessions come down to a weak connection, poor lighting, or a missing document rather than anything to do with the customer's identity.

Before beginning, make sure you have:

A device with a working camera and microphone

A stable internet connection and good lighting

Your identity document (for example, a passport, ID card, or in India a PAN card)

Permission for camera, microphone, and location access

No VPN and no face covering during the call

Benefits of Video KYC

Video KYC caught on because it serves two sides at once. For customers, it removes the friction of branch visits and paperwork; for the business, it turns a slow, costly compliance step into a fast digital one without giving up the assurance of a live check. The main benefits:

Full remote onboarding: complete a regulator-recognized KYC without a branch visit.

Speed and convenience: finished in minutes, from anywhere, often around the clock.

Higher conversion: replacing upload-only flows with a guided session reduces drop-off.

Lower fraud: a live check with liveness and an interview is harder to fake than a document upload.

Financial inclusion: reaches customers in remote areas who cannot easily visit a branch.

Is Video KYC Safe? Fraud and Deepfakes

Done properly, video KYC is as secure as an in-branch check, because it combines several defenses: end-to-end encryption, document authentication, face matching, and liveness detection, plus a human or AI reviewer and a full recording.

The main modern threat is deepfakes and injected video: an attacker feeding a synthetic face into the session through a virtual camera rather than showing it to a real one.

Strong video KYC counters this with active and passive liveness, gesture and depth challenges, document tilt checks, and injection detection.

Standard advice for customers: only use the official link, never share it, and be wary of any request to move the call to a third-party app.

Who Uses Video KYC?

Any business that has both a regulatory duty to verify customers and a reason to do it remotely is a candidate for video KYC.

In practice, adoption is highest in financial services, where a live, recorded check maps neatly onto strict onboarding rules, and it is spreading into any sector where the alternative is losing customers to a slow, in-person process.

The most common users:

Banks and neobanks (account opening)

Lenders and NBFCs (digital lending)

Insurance and wealth platforms

Crypto and trading platforms in regulated markets

Video Identity Verification with Qoobiss

Qoobiss supports compliant remote onboarding with document verification, NFC reading, biometric face matching, and liveness, the same building blocks that make a video KYC session trustworthy.

Whether you need a live agent-led flow, an automated one, or a hybrid, the platform captures the right evidence, defends against deepfakes and injection, and keeps a clean audit trail for regulators.

Frequently Asked Questions

What is video KYC?

How do you do video KYC at home?

What is the difference between KYC and video KYC?

Is video KYC safe?

What is V-CIP?

Is video KYC mandatory?