Money Laundering: What It Means, How It Works, and How It Gets Detected

The United Nations Office on Drugs and Crime estimates that between $800 billion and $2 trillion is laundered globally each year, a figure that represents 2% to 5% of global GDP. Less than 1% of those flows are intercepted. For regulated businesses, the implication is direct: money laundering is not a theoretical risk. It moves through banks, payment processors, real estate transactions, and digital asset platforms every day. The institutions that fail to detect it face regulatory penalties that now regularly reach into the billions.

Understanding how money laundering works, what techniques criminals use, and where the detection opportunities exist is foundational knowledge for any compliance team. This guide explains the money laundering definition, walks through its three stages, examines the most common laundering schemes with real-world examples, and covers how financial institutions identify and prevent illicit financial flows.

What Is Money Laundering?

Money laundering is the process of disguising the origins of illegally obtained funds so they appear to come from legitimate sources. The money laundering meaning, in both legal and regulatory usage, encompasses any financial transaction or series of transactions designed to conceal the true source, ownership, or destination of criminal proceeds.

The term itself dates back to the early twentieth century, when organized crime figures in the United States reportedly used cash-intensive businesses such as laundromats to commingle illicit revenue with legitimate income. The mechanism has grown far more sophisticated since then, but the underlying logic has not changed. Criminals who generate money through drug trafficking, fraud, corruption, human trafficking, tax evasion, or other predicate offenses cannot spend or invest that money openly without attracting attention from law enforcement and tax authorities. Money laundering solves that problem by creating a paper trail that makes dirty money look clean.

What does money laundering mean in practice? It can be as straightforward as a restaurant systematically overstating its cash receipts to absorb drug proceeds, or as complex as a multi-jurisdictional network of shell companies routing funds through correspondent banking channels in several countries before the money surfaces as a real estate investment. The methods vary enormously, but every money laundering scheme shares the same objective: create enough distance and complexity between the criminal act and the financial system that the funds become indistinguishable from legitimate wealth.

This is why anti-money laundering regulations exist. Every obligation placed on financial institutions, from customer due diligence to transaction monitoring to suspicious activity reporting, is designed to make that separation harder to achieve and easier to detect.

The Three Stages of Money Laundering

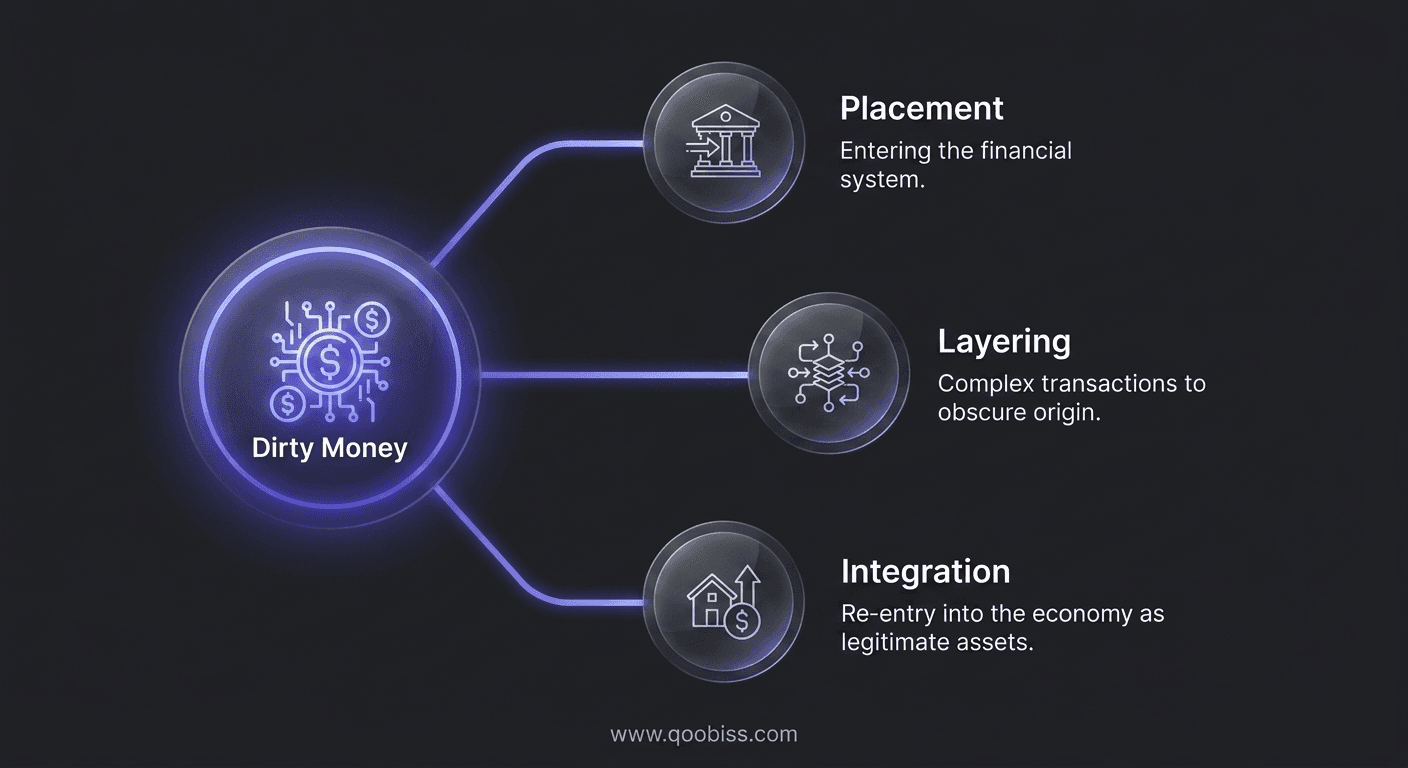

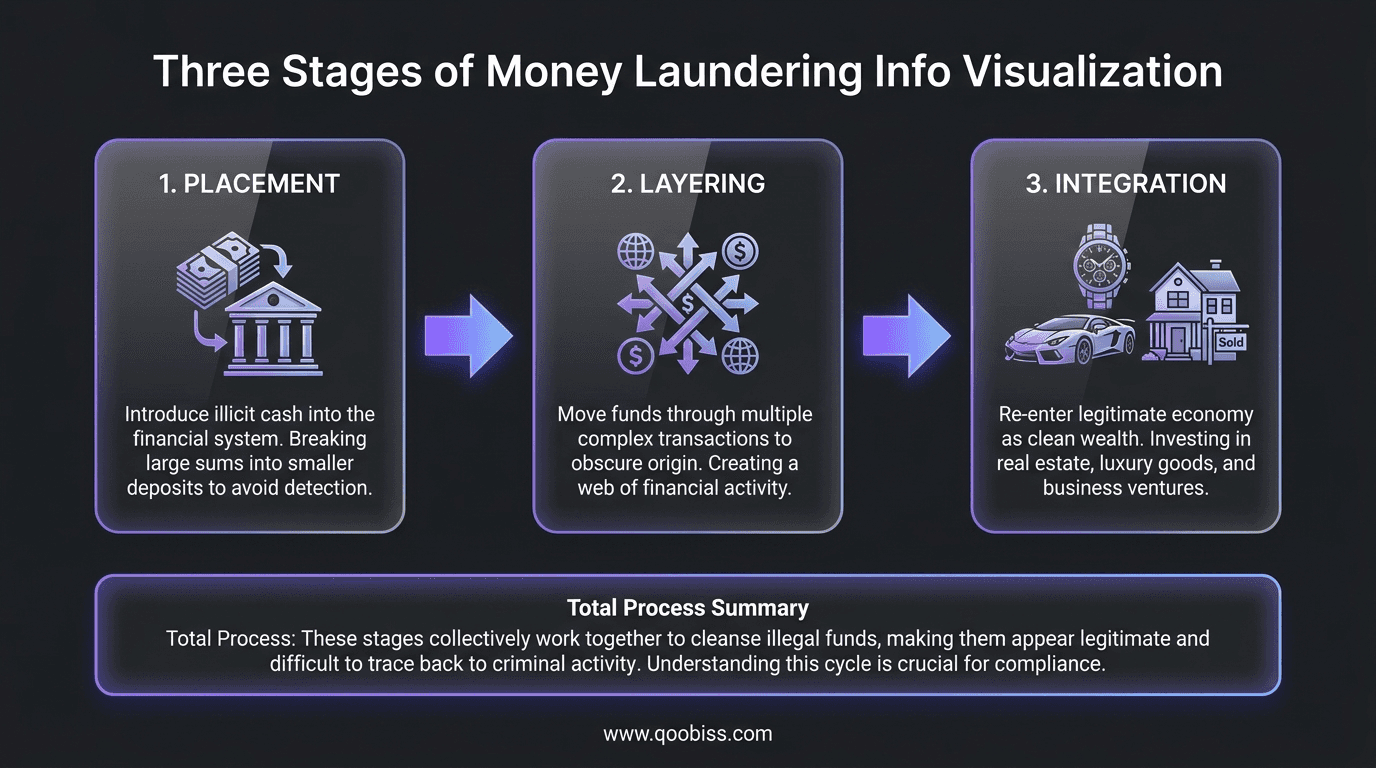

Money laundering is typically described as a three-stage process: placement, layering, and integration. In practice, laundering schemes rarely follow these stages in neat, sequential order. Elements of all three can overlap or occur simultaneously. But the framework remains useful for understanding how illicit funds move through financial systems and where institutions have opportunities to intervene.

Placement

Placement is the point at which illicit cash first enters the legitimate financial system. This is often the most vulnerable stage for criminals, because large volumes of unexplained cash are the most visible and easiest to flag.

Common placement techniques include structuring, also called smurfing, where large sums are broken into smaller deposits below reporting thresholds and spread across multiple accounts or branches. Cash-intensive businesses such as car washes, restaurants, parking garages, and retail shops provide another channel, allowing criminals to blend illegal cash with legitimate daily revenue. Currency exchange offices, gambling operations, and prepaid instruments also serve as placement vehicles, converting cash into less traceable forms.

Layering

Layering is the stage where criminals create complexity to obscure the audit trail. The goal is to put as many transactions and intermediaries between the original placement and the eventual use of funds as possible.

What is layering in money laundering terms? It is the deliberate creation of financial noise. Funds might move through a series of shell company accounts in different jurisdictions, be converted between currencies, pass through trade-based invoicing schemes that overstate or understate the value of goods, or cycle through securities purchases and sales. Wire transfers between banks in countries with weaker regulatory oversight are a common layering tool. Each additional layer of transactions makes it harder for investigators to trace the money back to its criminal origin.

Layering is where the sophistication of modern laundering schemes is most apparent. A single layering chain can involve dozens of entities across multiple countries, mixing legitimate and illegitimate transactions in ways that require significant analytical resources to untangle.

Integration

Integration is the final stage, where laundered funds re-enter the legitimate economy in a form that appears lawful. At this point, the money has been sufficiently distanced from its source that the criminal can use it without raising immediate suspicion.

Common integration methods include purchasing real estate, investing in businesses, buying luxury assets such as art, jewelry, or vehicles, and using loan-back arrangements where the criminal borrows their own laundered money from a foreign entity. Front companies that generate plausible revenue streams are another integration vehicle, providing an ongoing mechanism to absorb cleaned funds into the visible economy.

Common Money Laundering Schemes and Techniques

Beyond the three-stage framework, specific laundering techniques appear repeatedly across enforcement cases and regulatory guidance. Understanding these money laundering schemes helps compliance teams calibrate their monitoring and risk assessment models.

Trade-based laundering manipulates the price, quantity, or quality of goods in international trade transactions. An importer might overpay for a shipment of commodity goods, with the excess payment representing laundered funds sent to the exporter. The Financial Action Task Force has identified trade-based laundering as one of the most significant and least-detected channels for moving illicit value across borders.

Real estate laundering exploits the high transaction values, complex ownership structures, and historically limited transparency in property markets. Criminals purchase properties through shell companies or trusts, often in cash or through layered financing arrangements, then sell the properties to generate apparently legitimate proceeds.

Shell company structures allow criminals to own and move assets without their names appearing in any public record. Multiple layers of corporate ownership across jurisdictions with limited beneficial ownership disclosure requirements create opacity that is difficult for compliance teams to penetrate.

Cryptocurrency laundering uses the pseudonymous nature of blockchain transactions to move value quickly across borders. Techniques include chain-hopping between different cryptocurrencies, mixing services that pool and redistribute tokens, and peer-to-peer exchanges that bypass centralized compliance controls.

Hawala and informal value transfer systems operate outside the formal banking system entirely. Value is transferred through a network of brokers based on trust and mutual settlement, leaving little or no paper trail for regulators to follow.

Casino and gambling schemes convert cash into chips, conduct minimal play, then cash out and claim the proceeds as gambling winnings, providing a plausible explanation for the source of funds.

Round-tripping involves sending money abroad, often through jurisdictions with limited reporting requirements, and then bringing it back as a foreign investment or loan. The returning funds appear to originate from an overseas source, giving them a veneer of legitimacy that is difficult to challenge without detailed cross-border investigation.

Money Laundering Examples: Five Real-World Cases

Enforcement actions provide the clearest illustration of how these techniques operate at scale.

Danske Bank (2018). Investigators found that approximately €200 billion in suspicious transactions flowed through the bank’s Estonian branch between 2007 and 2015. Non-resident customers, primarily from Russia and former Soviet states, used the branch as a conduit for funds that passed through shell company accounts with little meaningful oversight. The case exposed systemic failures in correspondent banking due diligence and cost the bank billions in fines and settlements across multiple jurisdictions.

HSBC (2012). HSBC agreed to pay $1.9 billion to settle allegations that it failed to maintain an effective anti-money laundering program. The bank processed billions in transactions linked to Mexican drug cartels and sanctioned entities, including bulk cash shipments that were deposited directly at the bank’s Mexico branch. Compliance systems flagged transactions that were never investigated, and the bank’s AML staffing was grossly inadequate relative to its risk profile.

Wachovia / Wells Fargo (2010). Wachovia (later acquired by Wells Fargo) facilitated $378.4 billion in transactions connected to Mexican currency exchange houses between 2004 and 2007. Drug traffickers used the exchange houses to move narcotics proceeds into the US banking system. The bank paid $160 million in fines and forfeitures after admitting to anti-money laundering violations.

1MDB (2015–ongoing). The 1Malaysia Development Berhad scandal involved the misappropriation of over $4.5 billion from a Malaysian state investment fund. Laundered funds were used to purchase luxury real estate in New York and Los Angeles, finance a Hollywood film production, and acquire artwork and jewelry. The scheme spanned multiple countries and involved layering through offshore entities, Swiss bank accounts, and intermediary shell companies.

Westpac (2019). Australia’s financial intelligence agency, AUSTRAC, initiated civil proceedings against Westpac for more than 23 million breaches of anti-money laundering law. The breaches included failures to report international fund transfers and inadequate monitoring of transactions associated with possible child exploitation in Southeast Asia. Westpac agreed to a A$1.3 billion penalty, the largest in Australian corporate history at the time.

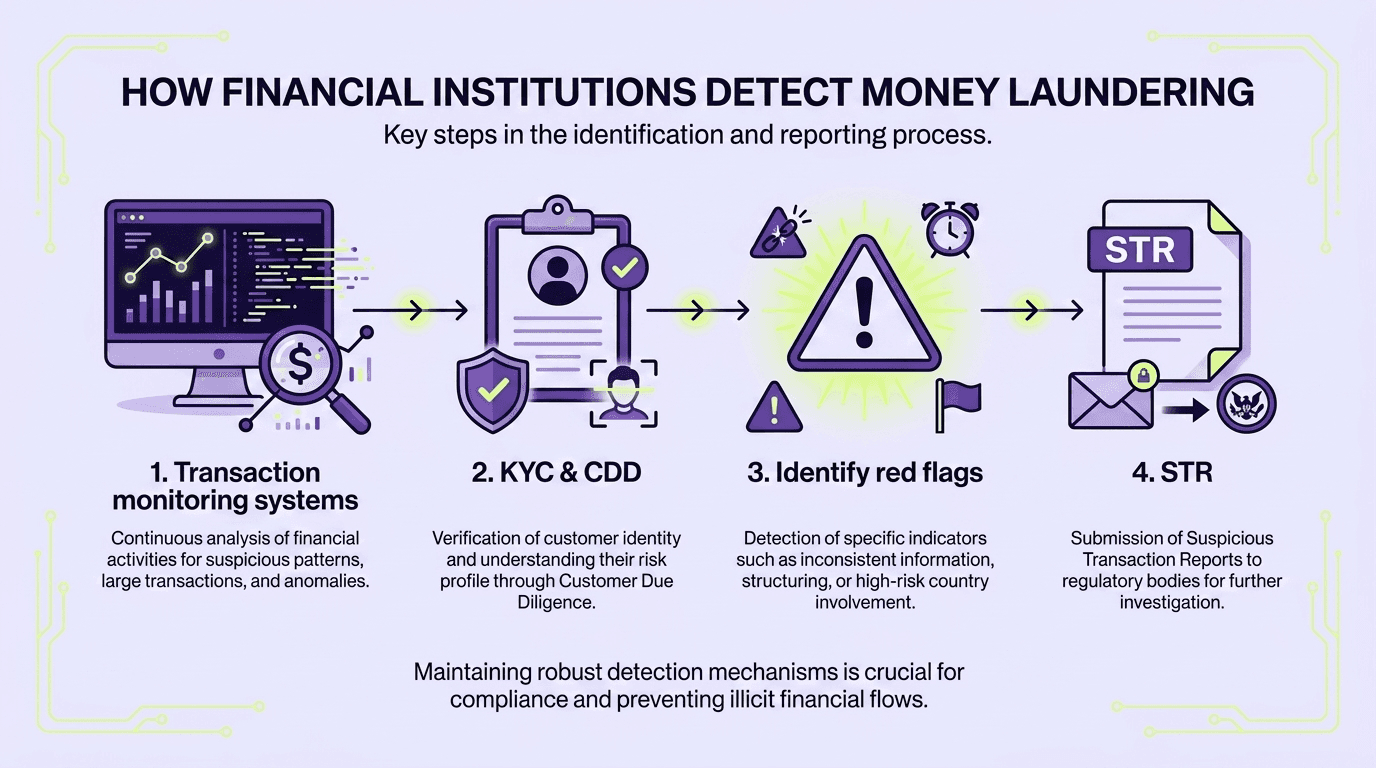

How Financial Institutions Detect Money Laundering

Detection starts before a customer makes a single transaction. Know Your Customer (KYC) and customer due diligence (CDD) processes establish the baseline against which all subsequent activity is measured. If an institution does not understand who the customer is, what their source of funds and wealth are, and what transaction patterns to expect, it has no foundation for identifying anomalies.

Transaction monitoring systems apply rules and, increasingly, machine learning models to flag activity that deviates from expected behavior. Common red flags include rapid movement of funds through accounts with no apparent business purpose, transactions structured just below reporting thresholds, high volumes of cash deposits followed by immediate wire transfers, and sudden changes in transaction patterns that are inconsistent with a customer’s profile or stated business activity.

When monitoring generates an alert, compliance teams investigate to determine whether the activity warrants a suspicious transaction report (STR) or suspicious activity report (SAR). The investigation process involves reviewing the customer’s transaction history, assessing the alert against known typologies, and documenting findings in a format that meets regulatory standards. Reports are filed with the relevant financial intelligence unit, such as FinCEN in the United States or the FIU in EU member states.

Sanctions and PEP screening add another detection layer, identifying customers or counterparties that appear on sanctions lists or hold politically exposed positions that elevate their risk profile. These screenings must run at onboarding and continuously throughout the relationship, because a customer’s risk status can change at any point due to new designations, political appointments, or adverse media coverage.

Correspondent banking relationships introduce additional risk, since financial institutions may process transactions on behalf of another bank’s customers without direct access to the underlying customer information. Effective correspondent banking due diligence requires understanding the respondent bank’s own AML controls, customer base, and jurisdictional risk exposure.

How Technology Is Changing Money Laundering Detection

Traditional rules-based transaction monitoring systems generate high volumes of false positives, often exceeding 95%. Compliance teams spend the majority of their investigative capacity reviewing alerts that turn out to be legitimate activity, which reduces the time available for genuine risk signals and creates operational drag that slows case resolution.

Machine learning models trained on historical case data can reduce false positive rates significantly by learning to distinguish between genuinely suspicious patterns and benign anomalies. Network analysis tools map relationships between entities, accounts, and transactions to reveal connections that would be invisible when looking at individual alerts in isolation. A single wire transfer may appear unremarkable, but when mapped against a web of related entities and transaction flows, it can reveal the layering structure of a laundering scheme.

Real-time screening against sanctions, PEP, and adverse media databases ensures that risk signals are identified at the point of transaction rather than days or weeks later during batch processing. Automated case management and workflow tools reduce manual effort in the investigation and reporting process, allowing compliance teams to focus on analysis rather than administrative tasks.

The shift from reactive, rules-based detection to proactive, data-driven intelligence is not optional for institutions operating at scale. Regulators increasingly expect institutions to demonstrate that their monitoring capabilities reflect the complexity of their risk exposure.

FAQ

What is money laundering in simple terms?

What are the 4 stages of money laundering?

What is an example of money laundering?

What is layering in money laundering?

How much money is laundered globally each year?

What is the difference between money laundering and fraud?

Qoobiss helps regulated businesses build the detection and compliance infrastructure that anti-money laundering obligations require. ONTRACE provides identity verification and KYC onboarding, establishing the customer due diligence foundation that effective monitoring depends on. OMNICHECK delivers real-time AML screening against sanctions, PEP, and adverse media databases. OVERWATCH unifies transaction monitoring, case management, and regulatory reporting into a single compliance operating environment. Request a demo to see how these modules work together to strengthen your AML program.