Digital Identity: How It Works and Why It Matters for Verification

Digital Identity: What It Is, How It Works, and Why It Matters for Verification

Every customer interaction that begins online, from opening a bank account to activating a mobile phone line to registering on a cryptocurrency exchange, requires establishing a digital identity. The concept has become so central to how businesses and governments operate that it now appears in regulatory frameworks, technology architectures, and fraud prevention strategies across every industry that handles personal data.

But digital identity means different things in different contexts. In IT security, it refers to the user profiles and credentials that control access to systems. In government policy, it refers to electronic citizen identity programs and digital ID wallets. For regulated businesses performing customer onboarding, digital identity has a more specific and operationally consequential meaning: the verified representation of a customer's real-world identity, established through document verification and biometric matching, that serves as the foundation for every subsequent compliance check, transaction, and risk decision.

This guide covers what digital identity is, the types of digital identities that exist, how digital identity verification works in practice, the frameworks and standards that govern it, the risks and threats businesses need to manage, and how digital identity applies across regulated industries.

What Is Digital Identity?

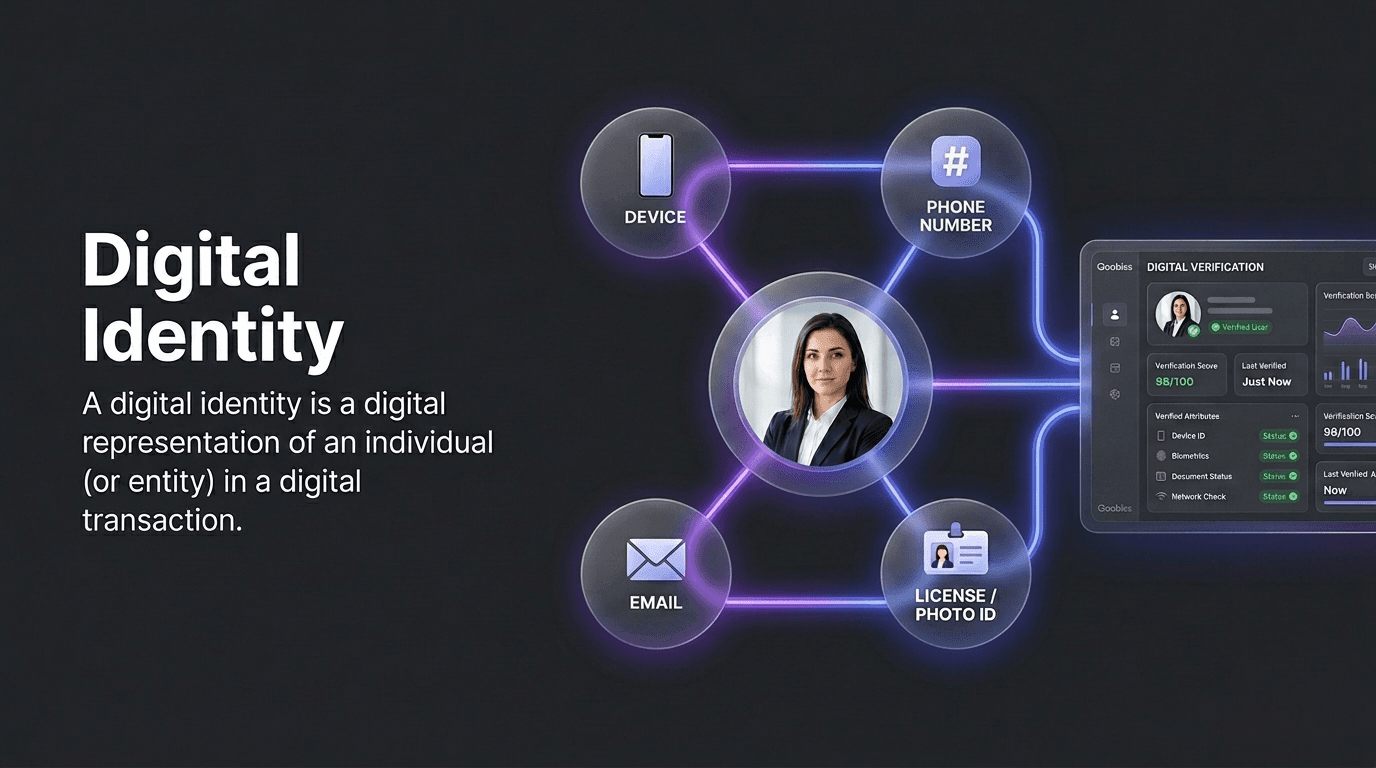

A digital identity is the collection of electronically captured and stored attributes that uniquely represent a person, organization, or device in digital systems. The digital identity definition encompasses everything from a name and date of birth linked to an online account to a cryptographically signed biometric template stored on an e-passport chip. In its simplest form, a digital identity answers a fundamental question: who or what is this entity in the digital environment?

The components that make up a digital identity fall into several categories. Personal identifiers include name, date of birth, nationality, and government-issued document numbers. Credentials are the authentication mechanisms tied to the identity, such as passwords, PINs, biometric templates, and cryptographic keys. Verified attributes are the results of identity proofing processes: the fact that a document has been authenticated, that a biometric match has been confirmed, that a sanctions screening has been cleared. Behavioral data, including login patterns, transaction history, and device fingerprints, can further enrich the identity over time.

A digital identity is not a single static record. It is a composite built from multiple sources and verified at different assurance levels depending on the use case. A social media profile establishes a low-assurance digital identity based on self-declared information. A bank account opened through a KYC process establishes a high-assurance digital identity backed by verified documents and biometric confirmation.

This distinction matters because the assurance level of a digital identity determines what it can be used for. Regulated businesses cannot rely on self-declared information. They need digital identities established through independent, verifiable evidence, which is where digital identity verification enters the picture.

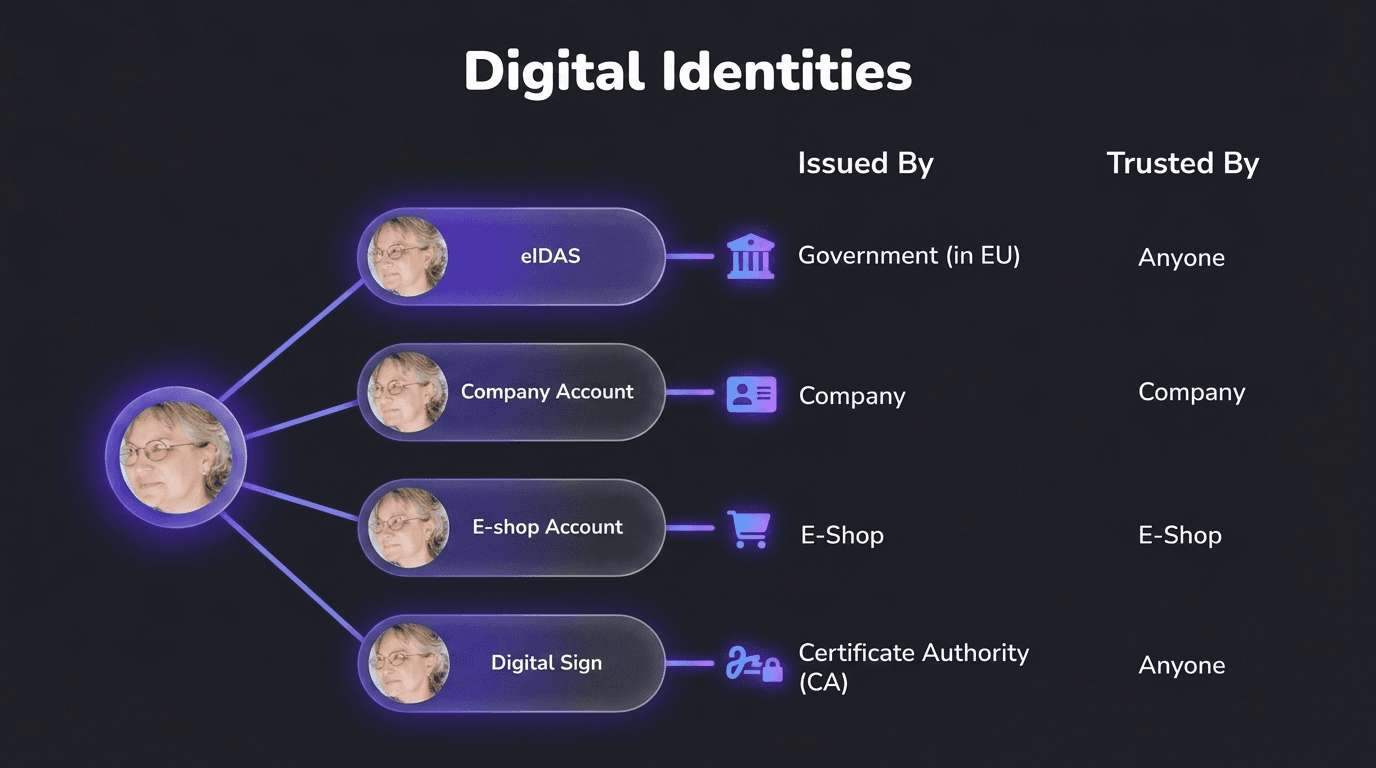

It is also worth distinguishing digital identity from digital ID. Digital identity is the broader concept: the full set of attributes and credentials that represent an entity digitally. A digital ID is a specific credential or token, such as a government-issued electronic identity card, a mobile driver's license, or an eIDAS-compliant digital wallet. A digital ID is one component of a digital identity, not the identity itself.

Types of Digital Identities

Personal Digital Identities

A personal digital identity is the set of attributes and credentials associated with an individual person. At the most basic level, this includes the account profiles people create when they register for online services: an email address and password, a username, profile information. These self-asserted identities carry low assurance because the information is not independently verified.

At higher assurance levels, personal digital identities are backed by government-issued credentials. National electronic identity cards, mobile driver's licenses, and digital identity wallets provide verified attributes that have been proofed against authoritative sources. The European Digital Identity Wallet, mandated by eIDAS 2.0, represents the current regulatory direction: a standardized, government-backed digital identity that citizens can use to authenticate themselves across public and private services throughout the EU.

For regulated businesses, the personal digital identity that matters is the one established during KYC onboarding, where the customer's real-world identity has been verified through document checks, biometric matching, and screening against sanctions and PEP databases.

Organizational Digital Identities

Organizations also maintain digital identities. A business registered with a national commercial registry has a legal identity that can be represented digitally through registration numbers, Legal Entity Identifiers (LEIs), and corporate KYC profiles. These organizational identities are essential for business-to-business relationships, correspondent banking, and beneficial ownership verification under AML regulations.

Machine and Device Identities

In connected environments, machines, devices, and software components also require digital identities. IoT devices authenticate using digital certificates. APIs use tokens and keys. Service accounts in cloud environments carry their own identity attributes. While machine identities operate differently from human identities, the underlying principle is the same: the system needs to establish what the entity is and what it is authorized to do.

In practice, these types interact constantly. A person uses a personal digital identity to access a service provided by an organization with its own verified identity, running on infrastructure secured by machine identities. The integrity of the entire chain depends on each identity being established and verified at the appropriate assurance level.

How Digital Identity Verification Works

Digital identity verification is the process of establishing that a claimed digital identity corresponds to a real person who is who they say they are. For regulated businesses, this process is not optional. KYC and AML regulations require that customer identity be verified using reliable and independent sources before a business relationship can be established.

The verification process follows a structured sequence, with each layer adding confidence to the identity being established.

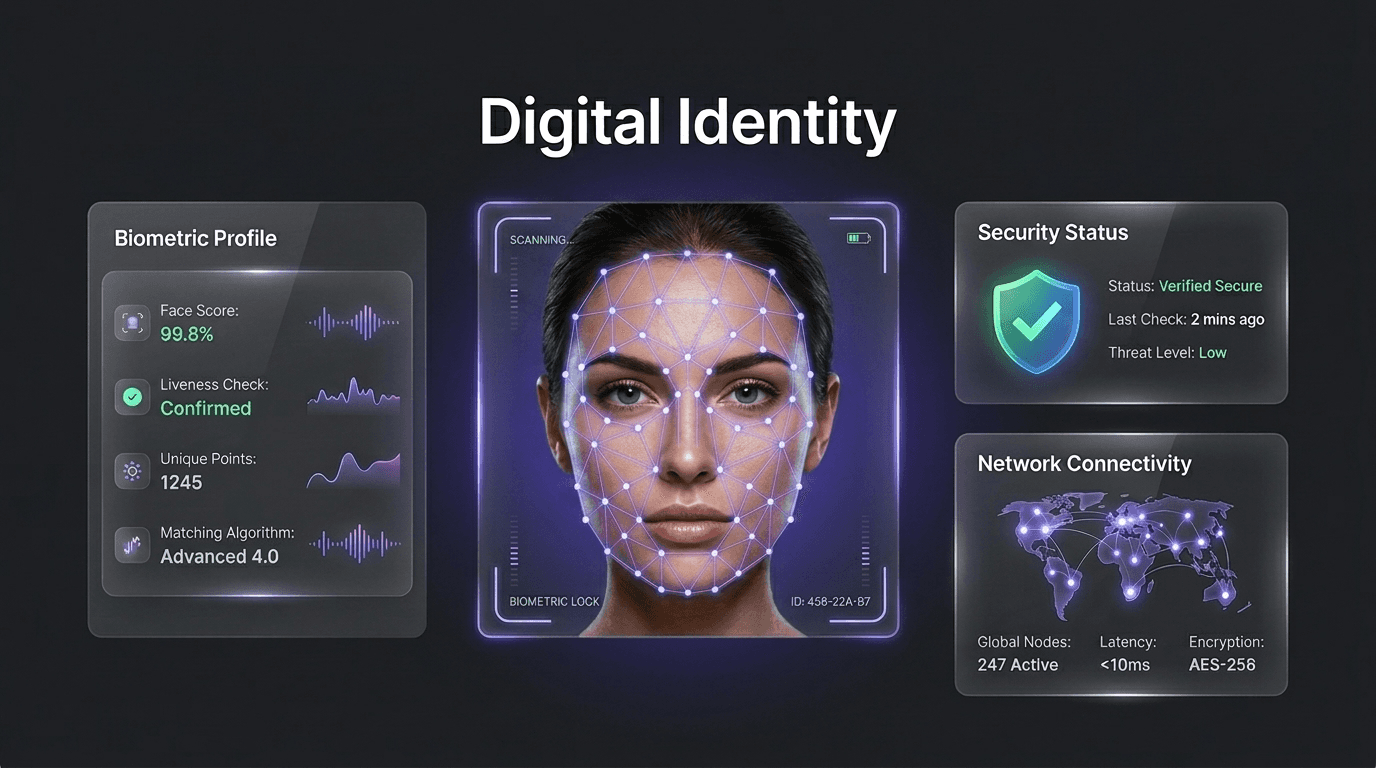

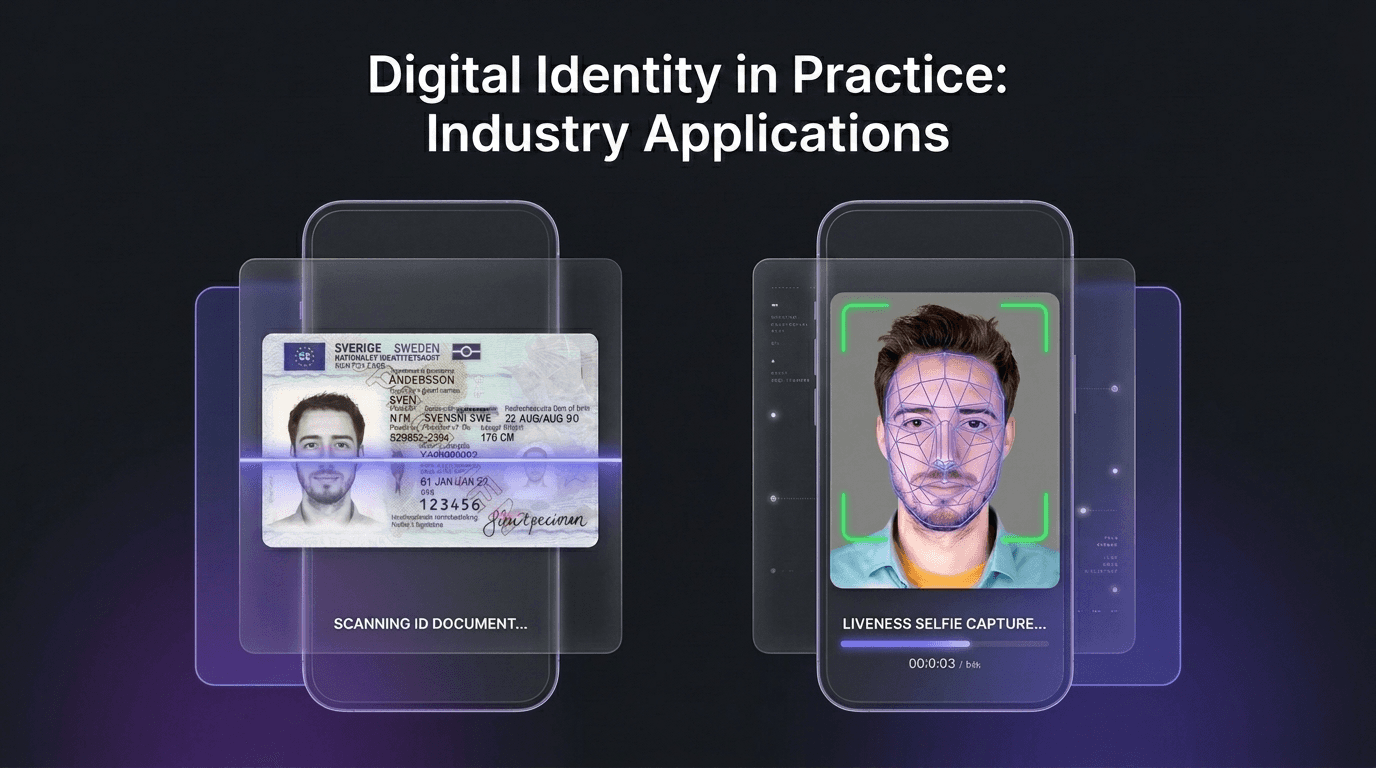

Document verification is the foundation. The customer submits a government-issued identity document, typically a passport, driver's license, or national ID card. The verification system captures an image of the document, extracts the personal data through optical character recognition (OCR), and analyzes the document against known templates for the specific document type and issuing country. Security features such as holograms, microprinting, UV-reactive elements, and MRZ formatting are checked for authenticity indicators.

Biometric matching confirms the link between the document and the person presenting it. The customer provides a live selfie, and the system compares the facial biometrics of the selfie against the photograph extracted from the identity document. This step answers a question that document verification alone cannot: is the person holding this document the person it was issued to?

Liveness detection ensures the biometric sample comes from a live person present at the time of verification, not from a photograph, pre-recorded video, or deepfake. Passive liveness detection analyzes texture, depth, and micro-movement characteristics without requiring the user to perform any specific action, keeping the process frictionless while defending against presentation attacks.

NFC chip reading provides the highest level of document authenticity assurance for chip-enabled documents. E-passports and many national ID cards contain NFC chips that store the holder's biometric data, signed with a cryptographic certificate from the issuing government. Reading and validating this chip data confirms document authenticity with certainty that no visual inspection or image analysis can match.

Data cross-referencing checks the verified identity against external risk databases: sanctions lists, politically exposed person (PEP) registries, adverse media sources, and where available, government document registries. This screening step ensures that the verified individual is not subject to restrictions that would prevent the business relationship from proceeding.

The output of this process is a verified digital identity: a customer record backed by authenticated documents, confirmed biometrics, and cleared screening results. This verified identity becomes the anchor for the entire customer relationship, supporting ongoing authentication, transaction monitoring, and periodic re-verification.

Digital Identity Frameworks and Standards

Several frameworks define the technical and governance requirements for digital identity systems. For regulated businesses, these frameworks establish the assurance levels that verification processes must meet.

NIST SP 800-63: Digital Identity Guidelines

The US National Institute of Standards and Technology publishes SP 800-63, the most widely referenced digital identity framework globally. The guidelines define three identity assurance levels (IALs) for identity proofing, three authenticator assurance levels (AALs) for authentication, and three federation assurance levels (FALs) for federated identity assertions. Each level specifies progressively stronger requirements. IAL2, for example, requires that identity evidence be verified against an authoritative source, while IAL3 requires in-person or supervised remote proofing with physical document inspection.

eIDAS 2.0 and the European Digital Identity Wallet

The EU's revised Electronic Identification, Authentication and Trust Services regulation (eIDAS 2.0) mandates that every EU member state offer citizens a European Digital Identity Wallet. These wallets will allow individuals to store verified identity attributes and present them to both public and private service providers across the EU. For businesses operating in Europe, eIDAS 2.0 introduces a standardized identity verification channel that carries government-backed assurance levels and interoperability guarantees across all member states.

ICAO Standards for Travel Documents

The International Civil Aviation Organization defines the standards for machine-readable travel documents through Document 9303 and related specifications. These standards govern the data structures, biometric formats, and cryptographic protocols used in e-passport NFC chips, and increasingly in Digital Travel Credentials (DTCs) that represent passport data on mobile devices. For identity verification providers, compliance with ICAO standards determines the ability to read and validate the chip data in over 150 countries' e-passports.

These frameworks do not operate in isolation. A regulated business onboarding customers internationally may need to satisfy NIST-level assurance requirements for US customers, accept eIDAS-compliant digital identities from EU customers, and validate ICAO-standard e-passports from customers worldwide. The verification platform must support all three.

Digital Identity Risks and Threats

The value of a verified digital identity makes it a high-priority target for fraud. The threats facing digital identity systems have grown more sophisticated as the technology used to establish and verify identities has advanced.

Identity theft and account takeover remain the most common attack vectors. Compromised credentials, whether obtained through phishing, data breaches, or social engineering, allow attackers to impersonate legitimate users and access their accounts. The Identity Defined Security Alliance has reported that over 80% of organizations have experienced at least one identity-related security incident.

Synthetic identity fraud is a growing threat that is particularly difficult to detect. Fraudsters combine real identity elements (such as a legitimate Social Security number) with fabricated information (a fake name and date of birth) to construct an entirely new identity that does not correspond to any real person. These synthetic identities can pass basic verification checks because some of the underlying data is genuine.

Document fraud targets the verification process directly. Counterfeit, altered, or digitally fabricated identity documents are submitted during onboarding to establish a fraudulent digital identity. AI-generated document images have raised the sophistication of this threat, producing synthetic documents that can pass basic template matching and OCR checks.

Deepfake and AI-generated biometric attacks target the biometric matching and liveness detection layers. Synthetic facial images and videos, generated using deep learning models, are presented during verification to impersonate real individuals or to match fraudulent document photos. Advanced liveness detection and deepfake detection models are the primary defense against this category of attack.

The common thread across these threats is that single-layer verification is insufficient. Each layer, document analysis, biometric matching, liveness detection, NFC chip validation, and data screening, addresses a different attack vector. Removing any one layer creates a gap that sophisticated fraud can exploit.

Digital Identity in Practice: Industry Applications

Financial services and fintech. Digital identity verification is the operational mechanism for KYC compliance in banking and financial services. Every new account, whether opened in a branch or through a mobile app, requires that the customer's identity be verified against a government-issued document. Remote digital onboarding has made this process faster and more accessible, but it has also required verification systems that can detect fraud without the benefit of physical document inspection.

Government services. National digital identity programs enable citizens to access government services electronically: filing taxes, accessing healthcare records, registering businesses, and voting. The EU's eIDAS 2.0 wallet initiative represents the most ambitious government-backed digital identity program currently in development, with the goal of providing every EU citizen with a universally accepted digital identity by 2026.

Telecommunications. SIM registration regulations in many jurisdictions require telecom operators to verify the identity of every subscriber. Digital identity verification enables this at scale, particularly in markets where the majority of activations happen through remote or self-service channels.

Healthcare. Patient identity verification prevents medical identity fraud and ensures that records, prescriptions, and insurance claims are associated with the correct individual. Digital identity solutions allow healthcare providers to verify patient identity during telehealth consultations and remote prescription services.

Crypto and Web3. Cryptocurrency exchanges and decentralized finance platforms are subject to KYC and AML regulations in most jurisdictions. Digital identity verification enables these platforms to comply with regulatory requirements while maintaining the remote-first, global user experience that their customers expect.

FAQ

What is digital identity in simple terms?

What is the difference between digital identity and digital ID?

Why is digital identity important for businesses?

How is digital identity verified?

What is a digital identity wallet?

Qoobiss provides the technology stack that regulated businesses need to establish and manage verified digital identities. ONTRACE handles identity verification at onboarding, combining document authentication, biometric facial matching, liveness detection, and NFC chip reading into a single verification flow. OMNICHECK screens verified identities against global sanctions lists, PEP databases, and adverse media sources. OVERWATCH provides ongoing transaction monitoring and case management, ensuring that the digital identity established at onboarding remains the basis for continuous compliance throughout the customer relationship.

Request a demo at qoobiss.com to see how Qoobiss supports your digital identity verification requirements.