Customer Identification Program (CIP): What It Is, Requirements, and How It Works

Customer Identification Program (CIP): What It Is, Requirements, and How It Works

Every bank account, brokerage account, and insurance policy opened in the United States begins with the same regulatory requirement. The financial institution must verify the identity of the person opening the account using procedures defined by federal law. This requirement, the Customer Identification Program, applies to every customer, every account, every time. It is not discretionary, and the consequences of noncompliance include regulatory penalties, enforcement actions, and the operational risk of onboarding customers whose identities have not been adequately verified.

The CIP requirement has been in effect since 2003, but the environment in which financial institutions fulfill it has changed fundamentally. Account opening has shifted from branch counters to mobile applications. Customer expectations have moved from multi-day processes to real-time onboarding. The volume and sophistication of identity fraud have increased dramatically. For financial institutions operating in this environment, understanding what CIP requires, how those requirements map to modern verification technology, and where CIP fits within the broader compliance framework is essential to building onboarding processes that are both compliant and operationally effective.

This guide covers what a customer identification program is, the specific requirements under federal regulation, the verification procedures institutions must implement, who must comply, how CIP relates to KYC and CDD, and how digital identity verification technology fulfills CIP obligations.

What Is a Customer Identification Program (CIP)?

A customer identification program is a written set of procedures that a financial institution uses to verify the identity of each customer who opens an account. The CIP requirement was established by Section 326 of the USA PATRIOT Act of 2001 and implemented through joint rulemaking by the US Department of the Treasury (through FinCEN) and the federal banking regulators. The implementing regulation, codified at 31 CFR 1020.220, became effective on October 1, 2003.

The regulatory intent is direct: financial institutions must form a reasonable belief that they know the true identity of each customer. This standard, "reasonable belief," is the operative threshold. The regulation does not require certainty. It requires that the institution's procedures, applied consistently, produce a well-founded confidence that the person opening the account is who they claim to be.

A CIP must be written, approved by the institution's board of directors, and incorporated into the institution's BSA/AML compliance program. The program must be proportionate to the institution's size, type of business, and risk profile. A community bank with a local customer base will have different CIP procedures than a multinational financial institution onboarding customers across multiple jurisdictions, but both must meet the same minimum regulatory requirements.

It is important to understand where CIP sits within the broader compliance hierarchy. CIP is not synonymous with KYC. It is one component of KYC, specifically the identity verification component that operates at the point of account opening. CIP establishes who the customer is. Customer Due Diligence (CDD) builds on the identity established by CIP to assess the customer's risk profile, understand the nature and purpose of the business relationship, and identify beneficial owners of entity accounts. Ongoing monitoring then uses the baseline established by CDD to detect suspicious activity throughout the customer lifecycle. CIP is the foundation on which the rest of the KYC framework is built.

CIP Requirements: The Four Required Data Elements

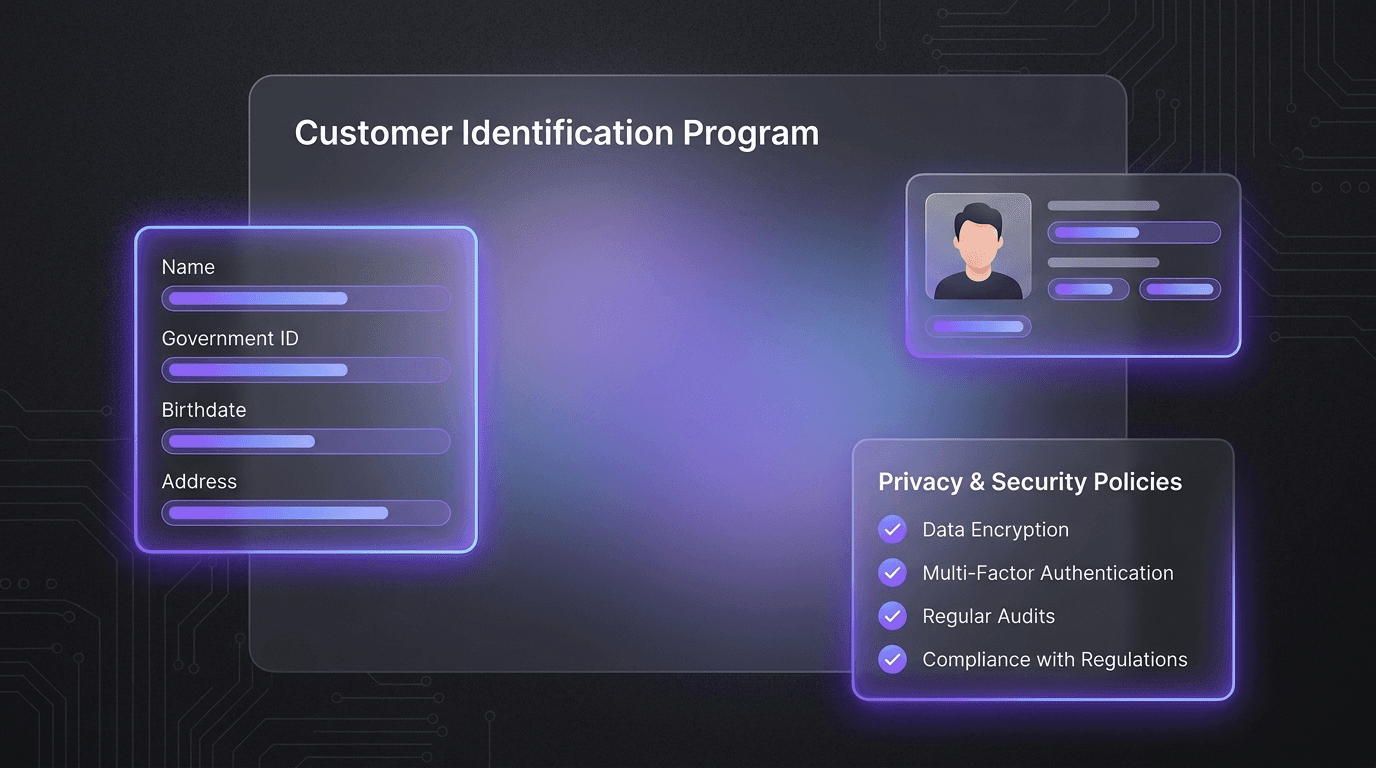

Under 31 CFR 1020.220, financial institutions must collect four pieces of identifying information from each individual customer before opening an account.

Name

The customer's full legal name. This is the name as it appears on the customer's government-issued identification and serves as the primary identifier for all subsequent verification, screening, and recordkeeping.

Date of Birth

The customer's date of birth. This requirement applies to individual customers. Entity accounts (corporations, trusts, partnerships) are not required to provide a date of birth but must provide other identifying information appropriate to the entity type, including principal place of business, employer identification number, and formation documents.

Address

A residential or business street address. For individuals who do not have a street address, the regulation accepts alternative documentation: a military APO or FPO address, the address of a next of kin or another contact individual, or a description of the customer's physical location. For entity accounts that are not physically located in the United States, the regulation accepts a principal place of business, local office, or other physical location.

Identification Number

For US persons, a taxpayer identification number, which is typically a Social Security number for individuals or an employer identification number for entities. For non-US persons, the institution must collect one or more of the following: a taxpayer identification number, a passport number and country of issuance, an alien identification card number, or the number and country of issuance of any other government-issued document that evidences nationality or residence and contains a photograph.

These four elements are the regulatory minimum. Financial institutions may, and frequently do, collect additional information based on their own risk assessment. The nature and purpose of the account, the source of funds, and additional contact information are commonly collected alongside the four required elements to support the institution's CDD process.

Identity Verification Procedures

Collecting the four data elements is only the first step. The CIP must also include risk-based procedures for verifying the identity of each customer "to the extent reasonable and practicable." The regulation provides two categories of verification methods.

Documentary Verification

Documentary verification involves examining a government-issued document that bears a photograph and identifies the customer by name, date of birth, and address. For individuals, the most common documents are an unexpired driver's license, passport, or national ID card. For entities, acceptable documents include certified articles of incorporation, a government-issued business license, a partnership agreement, or a trust instrument.

The regulation recognizes that no document is immune to fraud. The CIP Final Rule explicitly states that institutions are not required to determine the authenticity of every document presented. The standard is that the institution's procedures, taken as a whole, enable it to form a reasonable belief that it knows the customer's true identity.

Non-Documentary Verification

Non-documentary verification uses methods that do not require physical document presentation to verify identity. These methods include contacting the customer directly, comparing the identifying information provided against consumer reporting agency databases, checking references with other financial institutions, and obtaining financial statements or other confirming documentation.

The regulation requires institutions to use non-documentary methods in specific circumstances: when the customer is not physically present at account opening (which includes all remote and digital onboarding), when the institution cannot examine the document, when there are concerns about document authenticity, or when the institution cannot verify the type of identifying information required.

This distinction between documentary and non-documentary verification is operationally significant because it is the regulatory basis for digital identity verification. The CIP Final Rule was drafted in 2003, but its technology-neutral, risk-based framework was designed to accommodate verification methods beyond in-person document inspection. The regulation does not prescribe specific technologies. It requires that the institution's procedures produce a reasonable belief in the customer's identity, regardless of the channel through which the account is opened.

Recordkeeping and Retention

The CIP rule imposes specific recordkeeping requirements. The institution must retain the identifying information collected at account opening (name, date of birth, address, identification number) for five years after the record is made. Additionally, the institution must retain for five years after the account is closed: a description of the documents relied upon for verification (including document type, identifying number, place of issuance, and expiration date), a description of any non-documentary methods used, the results of any measures taken to verify identity, and a description of the resolution of any discrepancy in the identifying information.

These retention requirements mean that the CIP process must produce a verifiable audit trail. Every verification decision, whether based on documentary or non-documentary methods, must be recorded in sufficient detail to demonstrate compliance during a regulatory examination. For institutions performing manual, paper-based verification, this creates a significant administrative burden. For institutions using digital identity verification, the verification record is generated automatically as part of the process, typically capturing the document images, the verification results, the biometric matching score, and a timestamped audit log.

CIP Notice Requirements

The CIP rule requires financial institutions to provide customers with adequate notice that information is being requested to verify their identity. The notice must be provided before or at the time of account opening. FINRA has published model notice language that institutions may adopt or adapt, which informs the customer that federal law requires the institution to obtain, verify, and record information that identifies each person who opens an account.

The notice requirement is a transparency obligation. It ensures that customers understand why they are being asked to provide identifying information and documents, reducing friction during the onboarding process and setting expectations about the verification steps that will follow.

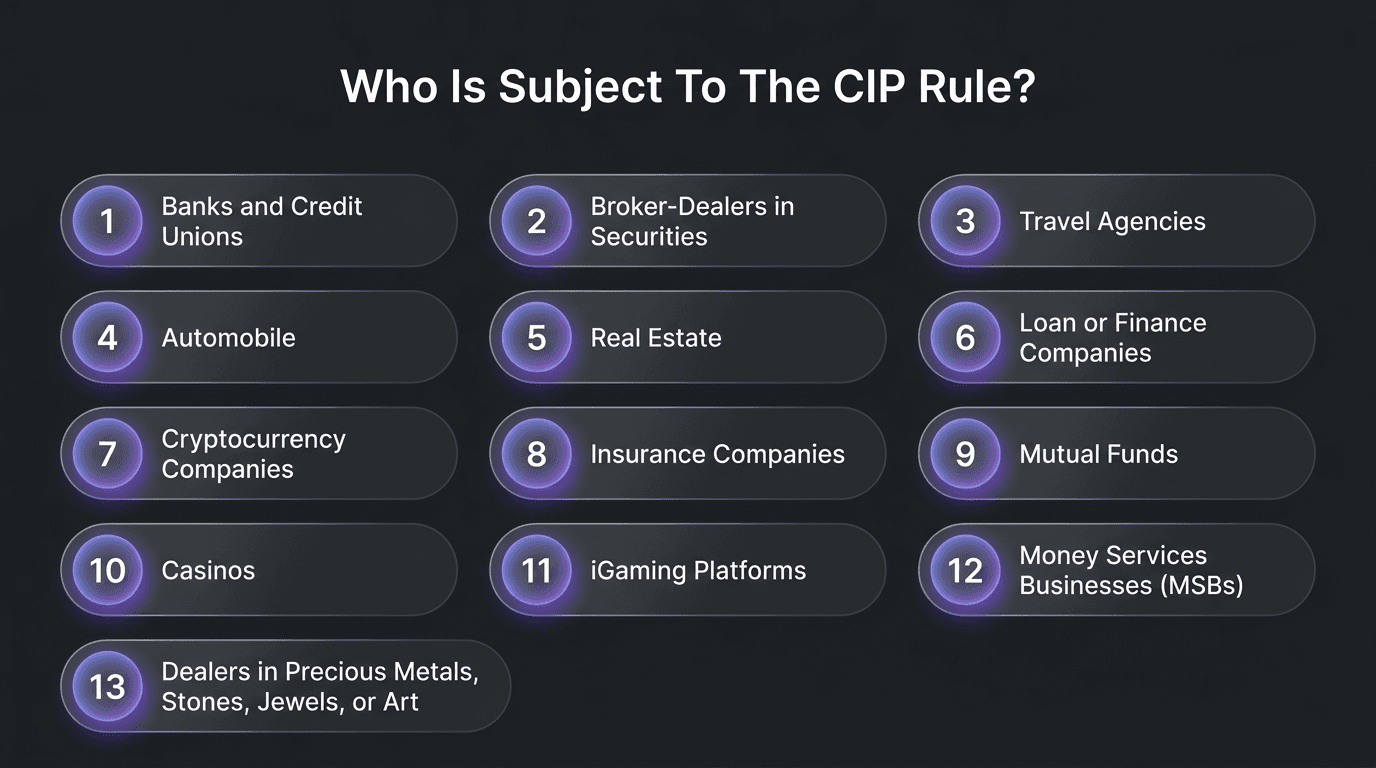

Who Must Comply with CIP Rules?

Banks and Credit Unions

All federally regulated depository institutions are subject to the CIP requirement under 31 CFR 1020.220. This includes national banks, state-chartered banks, savings associations, and credit unions. The CIP must be integrated into the institution's BSA/AML compliance program and is subject to examination by the institution's primary federal regulator.

Broker-Dealers

Securities broker-dealers are subject to CIP requirements under SEC Rule 17a-8 and FINRA regulations. The CIP requirements for broker-dealers closely parallel those for banks, including the four required data elements, documentary and non-documentary verification procedures, and recordkeeping obligations.

Insurance Companies

Insurance companies that issue or underwrite certain covered products are subject to CIP requirements. The scope of what constitutes a "customer" and an "account" varies by product type. Permanent life insurance policies, annuity contracts, and other products with investment characteristics generally trigger CIP obligations.

Other Financial Institutions

FinCEN has extended CIP and CIP-equivalent requirements across the financial sector, including money services businesses, mutual funds, futures commission merchants, and commodity trading advisors. The specific requirements vary by institution type, but the core principle is consistent: before establishing a business relationship, the institution must verify the customer's identity using procedures appropriate to its risk profile.

CIP vs. KYC vs. CDD

These three terms are frequently conflated, but they describe distinct components of a compliance framework with different scopes and timing.

CIP is identity verification at account opening. It answers the question: who is this customer? The institution collects the four required data elements and verifies them through documentary or non-documentary methods. CIP is a point-in-time process that occurs when the account is established.

Customer Due Diligence builds on the identity established by CIP to assess risk. CDD includes understanding the nature and purpose of the customer relationship, developing a customer risk profile, and, for entity accounts, identifying and verifying beneficial owners who hold 25 percent or more of the equity interest. FinCEN's 2016 beneficial ownership rule formalized this requirement, and subsequent rulemaking under the Corporate Transparency Act has further expanded beneficial ownership reporting obligations.

Ongoing monitoring uses the baseline established by CDD to detect anomalies throughout the customer lifecycle. Transaction monitoring systems flag activity that is inconsistent with the customer's risk profile. Periodic reviews update the customer's risk assessment. Suspicious activity reporting obligations are triggered when monitoring identifies transactions that may involve illicit funds.

The relationship is sequential and cumulative. CIP provides the verified identity. CDD uses that identity to assess risk. Ongoing monitoring ensures the risk assessment remains current. Weaknesses at the CIP stage compromise everything that follows: if the customer's identity was not properly verified, the risk assessment is built on an unreliable foundation, and monitoring may be calibrated against a fictitious profile.

How Technology Fulfills CIP Obligations

The CIP Final Rule was written when most account openings occurred at a branch counter, with a bank employee physically inspecting a customer's driver's license or passport. The regulation's technology-neutral, risk-based framework has allowed it to accommodate digital identity verification methods that produce equal or superior assurance compared to in-person inspection.

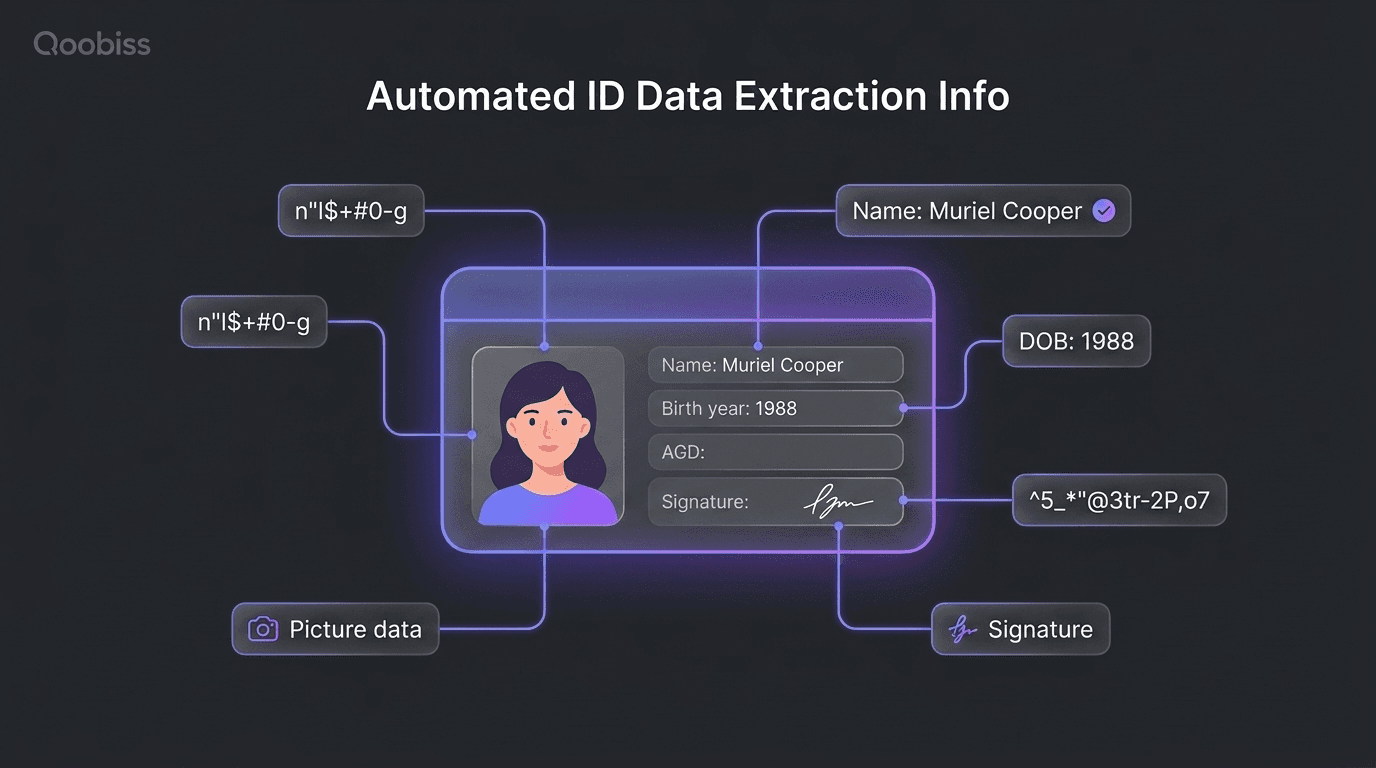

Document verification technology captures an image of a government-issued identity document, extracts the four required data elements through OCR, and authenticates the document through template matching, security feature analysis, and consistency checks. This satisfies the documentary verification requirement while producing a digital verification record that meets the CIP's recordkeeping obligations automatically.

Biometric facial matching compares a live selfie to the photograph on the submitted identity document, confirming that the person opening the account is the person the document was issued to. This addresses a verification gap that physical document inspection struggles to close: a bank teller comparing a customer's face to a small photograph on a driver's license is performing a subjective visual assessment, while a biometric matching algorithm produces an objective, quantified similarity score.

NFC chip reading, for chip-enabled documents such as e-passports and many national ID cards, reads the biographic and biometric data stored on the document's NFC chip and validates the cryptographic signature issued by the document's issuing government. This level of document authentication exceeds what any visual or physical inspection can achieve, because the cryptographic signature confirms document authenticity with mathematical certainty.

Non-documentary verification through automated database screening checks the customer's identifying information against consumer reporting agency databases, government registries, and sanctions and PEP lists. This satisfies the non-documentary verification requirements of the CIP rule while simultaneously feeding into the CDD risk assessment process.

The combination of these methods produces a CIP verification record that meets the regulatory standard of "reasonable belief" while delivering a faster, more consistent, and more auditable process than manual verification. For institutions operating digital onboarding channels, these technologies are not optional enhancements. They are the operational mechanism through which CIP compliance is achieved at scale.

FAQ

What is a customer identification program in simple terms?

What are the four elements of a customer identification program?

What is the difference between CIP and KYC?

Who is required to have a customer identification program?

Can CIP verification be completed remotely?

What records must be retained under CIP?

Qoobiss provides the technology infrastructure that enables financial institutions to fulfill CIP obligations through digital channels. ONTRACE handles identity verification at account opening: document verification extracts the four required data elements and authenticates document genuineness through template matching and security feature analysis. Biometric facial matching confirms the customer is the document holder. NFC chip reading validates cryptographically signed data from e-passports and chip-enabled national ID cards, providing document authentication that exceeds the assurance level of physical inspection.

OMNICHECK screens verified identities against global sanctions lists, PEP databases, and adverse media sources, fulfilling non-documentary verification requirements while feeding into the broader CDD risk assessment. Every verification produces a timestamped, auditable record that satisfies CIP recordkeeping obligations.

Request a demo at qoobiss.com to see how Qoobiss supports CIP compliance across your onboarding channels.