What Is KYB (Know Your Business)? Verification Requirements Explained

Know Your Business (KYB) is the process of verifying a company's legal identity, ownership structure, and risk profile before onboarding it as a customer or partner.

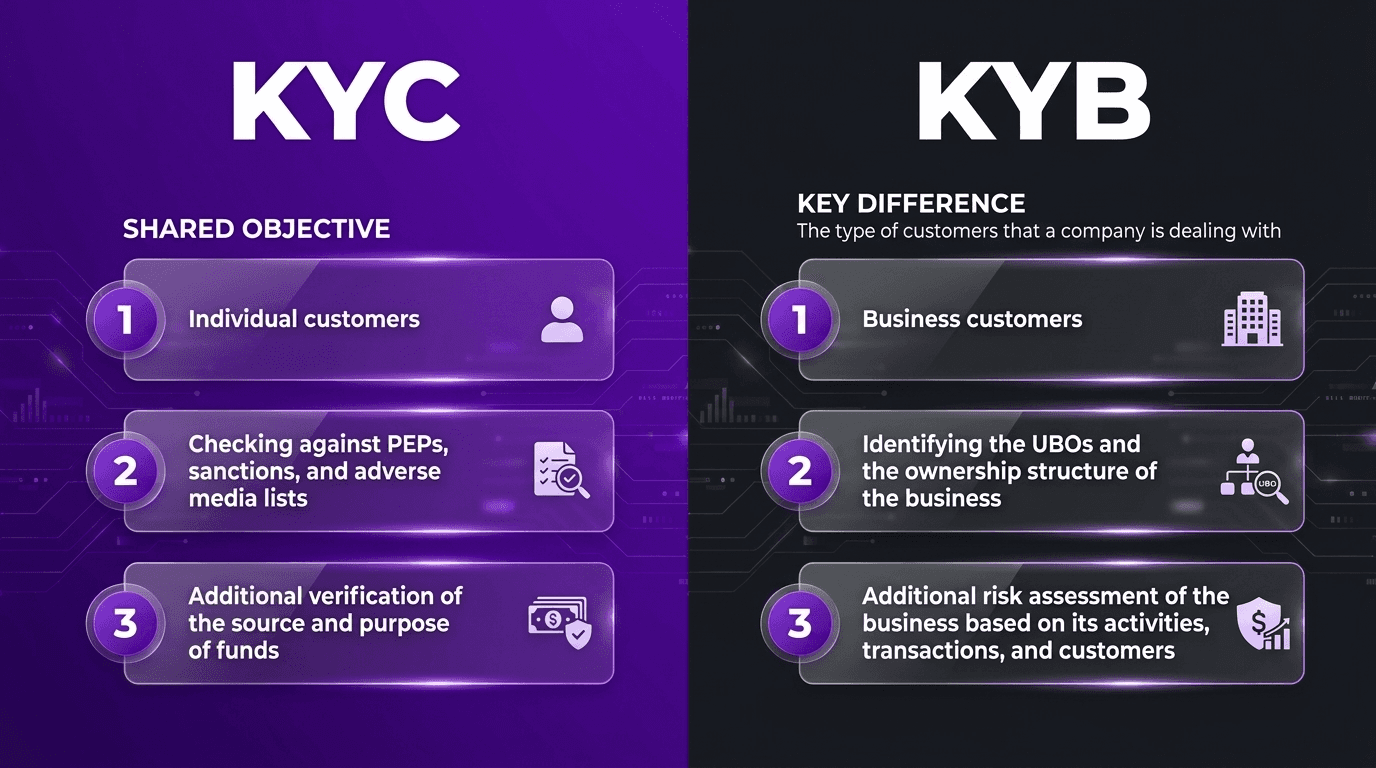

Where KYC (Know Your Customer) verifies individuals, KYB confirms that a business genuinely exists, identifies the real people who own and control it, and checks whether it presents a compliance or fraud risk. In short, KYB is KYC applied at the company level, with extra layers of complexity.

This guide explains what KYB is, how it differs from KYC, the documents and checks it requires, how ultimate beneficial owners fit in, the regulations behind it, and how the process works.

The core purpose of KYB is to stop criminals from hiding behind a company. A shell company, a business with no real operations set up as a front, is one of the most common vehicles for money laundering, sanctions evasion, and fraud.

KYB pierces that veil by confirming the business is legitimate and identifying the humans behind it. It is a regulatory requirement for banks, fintechs, payment providers, and other regulated firms before they open accounts, extend credit, or process payments for a business customer.

The cost of getting it wrong is steep: reported AML penalties reached over $1 billion in the first half of 2025 alone, and individual banks have faced multi-billion-dollar fines for failures (industry reporting).

KYB vs KYC: What Is the Difference?

KYB and KYC share the same goal, verifying identity and managing risk, but they apply to different subjects and demand different depth.

Factor | KYC (Know Your Customer) | KYB (Know Your Business) |

|---|---|---|

Subject verified | An individual | A business entity, plus its owners |

Documents | Personal ID, proof of address, selfie | Registration filings, tax ID, ownership records, licenses |

Data sources | ID documents, biometrics, databases | Company registries, plus KYC on individuals |

Ownership layer | None | Must identify and verify ultimate beneficial owners (UBOs) |

Complexity | Simpler, one person | Higher, entity plus every controlling individual |

Typical timeline | Minutes to hours | Hours to several weeks |

Used for | Retail banking, consumer apps, crypto | Corporate banking, B2B, marketplaces, merchant onboarding |

The two are not either/or. KYB verifies the business entity and then runs KYC checks on its directors and beneficial owners, so a complete business onboarding uses both.

KYB Verification Requirements: The Document Checklist

The exact requirements vary by jurisdiction and risk level, but a KYB check typically collects and verifies the following:

Requirement | What it confirms |

|---|---|

Legal business name & registration number | The entity is registered and exists in an official registry |

Certificate of incorporation / formation | Legal formation of the company |

Registered address & proof of address | A real, verifiable place of business (not just a mail drop) |

Tax identification (EIN, VAT, or equivalent) | The company's tax registration |

Articles of association / bylaws | Governance, and who has authority |

Ownership & shareholder registry | Ownership percentages and structure |

Ultimate beneficial owners (UBOs) | The individuals who ultimately own or control the business |

Directors and authorized signatories | The people who run and can act for the company (verified via KYC) |

Operating licenses & permits | Authorization to carry out the stated business activities |

Sanctions, PEP & adverse media screening | That the business and its principals are not high-risk or restricted |

Ultimate Beneficial Owners (UBOs): The Heart of KYB

An ultimate beneficial owner is the real person who ultimately owns or controls a business. Regulations typically define a UBO as anyone who holds more than 25% of ownership or exercises significant control over the company, even if that control runs through layers of holding companies or trusts.

Because criminals use layered ownership to hide, identifying UBOs is the single most important part of KYB. Once a UBO is identified, they are verified using the same standards as an individual KYC check and screened against sanctions and PEP lists. For a deeper look, see our guide to the ultimate beneficial owner.

Beneficial ownership registers. Regulators increasingly require ownership to be recorded centrally. EU anti-money-laundering directives require member states to maintain central beneficial ownership registries, and in the US the Corporate Transparency Act requires many companies to report beneficial ownership information (BOI) to FinCEN. (The scope and status of US BOI reporting has changed recently, so confirm current requirements.)

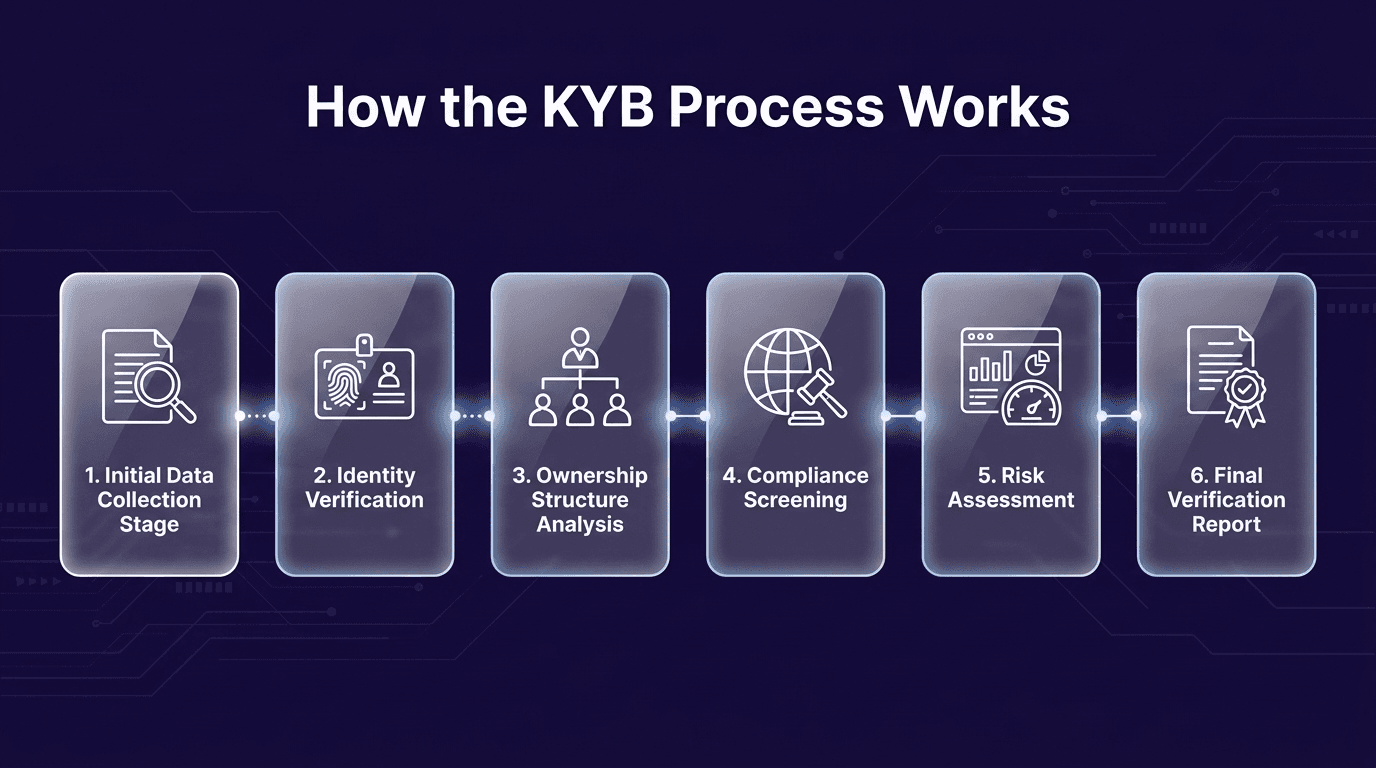

How the KYB Process Works

A typical KYB verification follows these steps:

Collect business information. Legal name, registration number, registered address, and industry classification.

Verify the entity exists. Cross-reference against official government registries and confirm the company is in good standing.

Map the ownership structure. Identify all owners, shareholders, and parent entities, with ownership percentages.

Identify the UBOs. Pinpoint individuals with more than 25% ownership or significant control.

Run KYC on key individuals. Verify directors, authorized signatories, and UBOs, and check source of funds where relevant.

Screen for risk. Check the business and its principals against sanctions, PEP, and adverse media sources.

Risk-rate and monitor. Assign a risk score, apply enhanced due diligence to higher-risk cases, and monitor for changes on an ongoing basis.

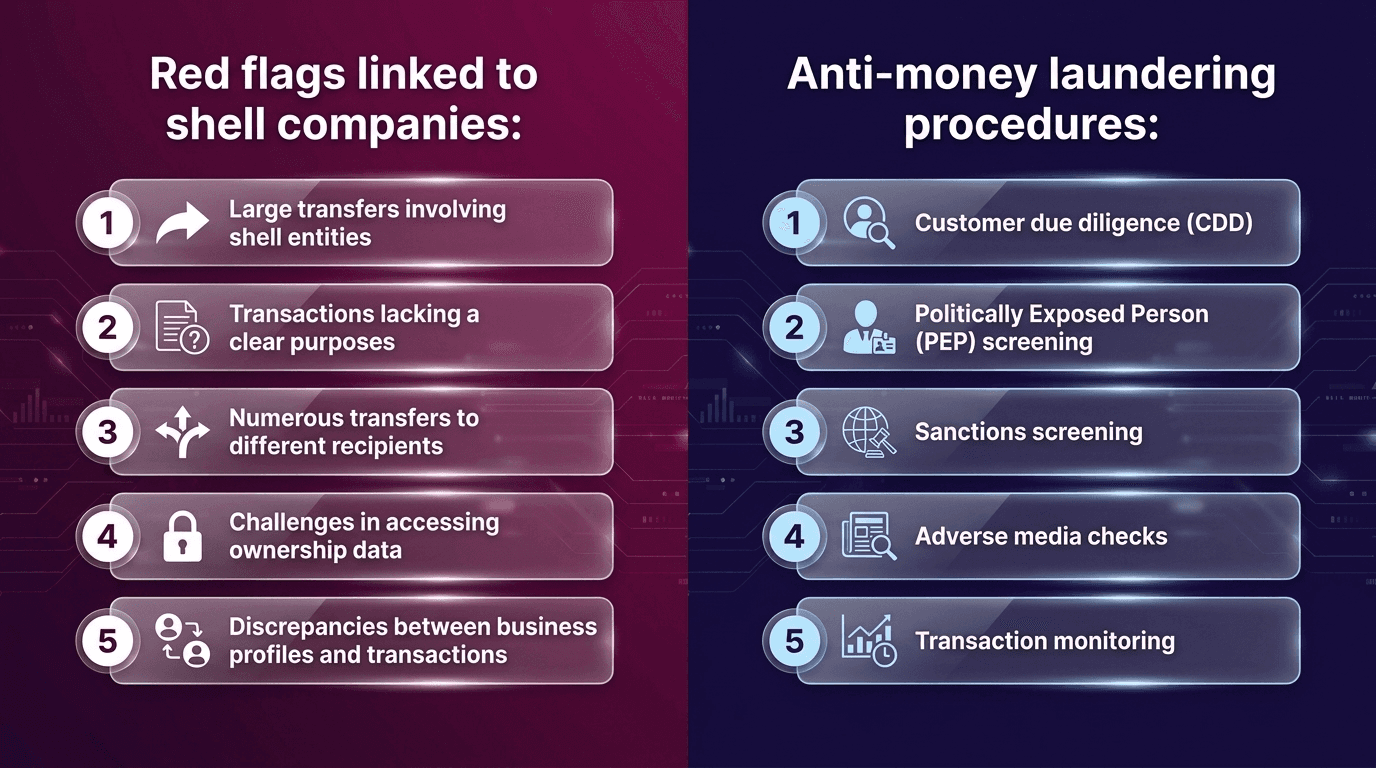

Shell-Company Red Flags to Watch For

During KYB, treat the following as signals that a business needs closer scrutiny:

A registered address that is a mail drop or virtual office with no real operations

Complex, multi-layered ownership with no clear business rationale

Reluctance to disclose owners or provide documentation

Incorporation in a high-risk or secrecy jurisdiction inconsistent with the business

Inconsistent or altered documents, or names that nearly match sanctioned parties

Unusual urgency to onboard or activity that does not match the stated business

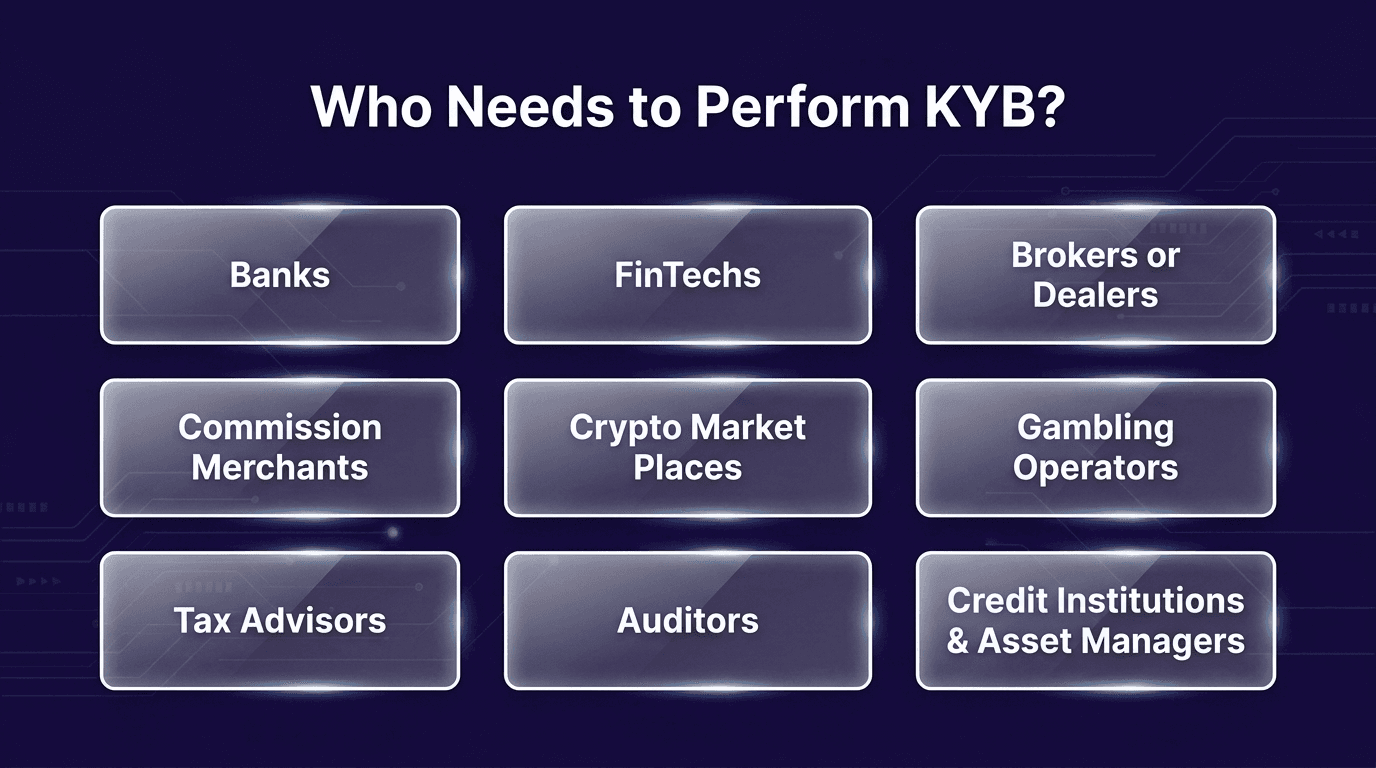

Who Needs to Perform KYB?

Any regulated business that onboards other businesses needs KYB. Common cases include:

Banks and lenders: opening corporate accounts or extending commercial credit.

Fintechs and payment providers: onboarding merchants for payment processing.

Marketplaces and platforms: verifying sellers, vendors, and suppliers.

Crypto and digital-asset firms: onboarding institutional or business clients.

B2B SaaS and BaaS providers: verifying business customers and, sometimes, their customers.

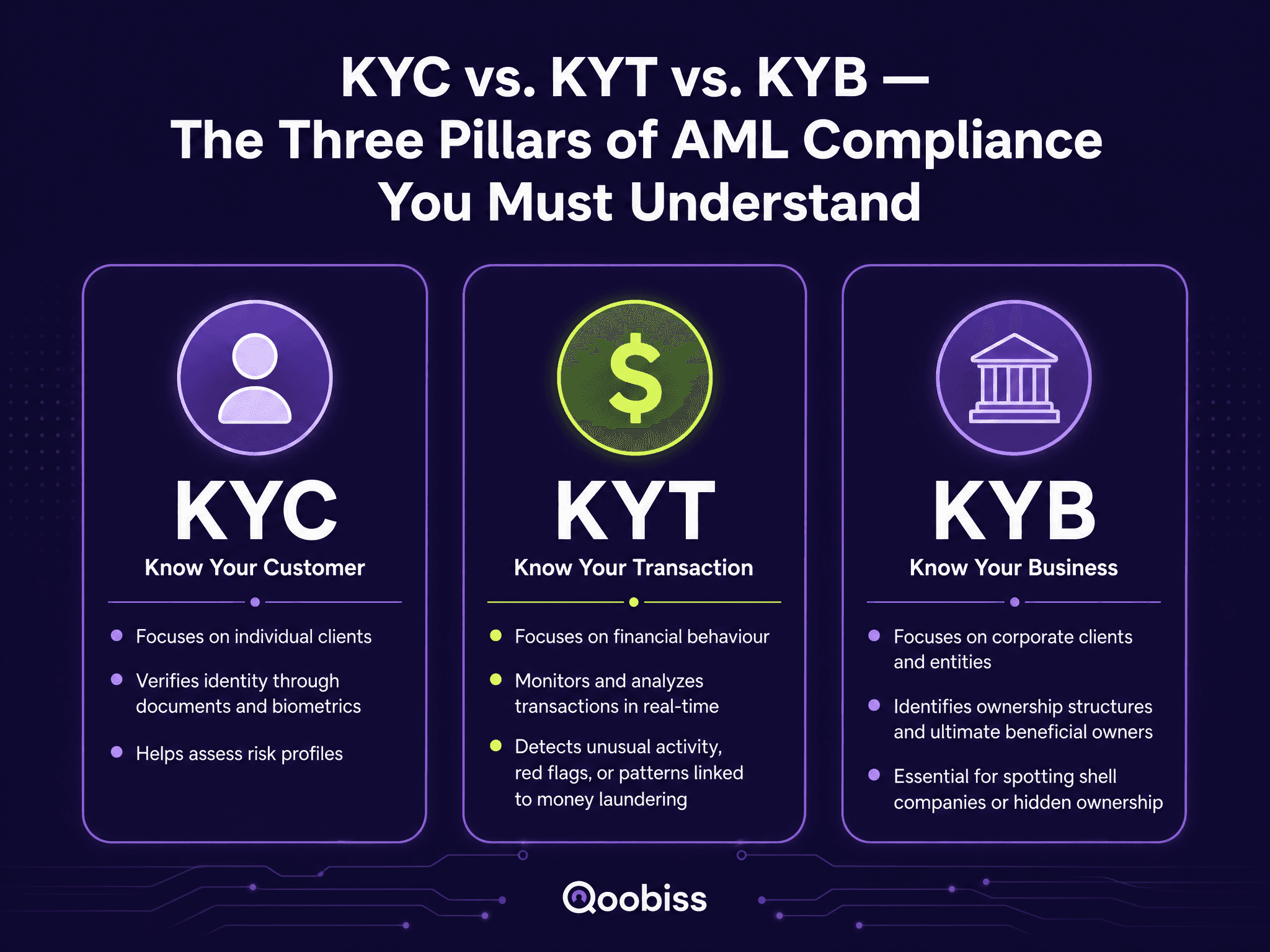

KYB, KYC, KYT: How the Terms Fit Together

Compliance is full of similar-looking acronyms, and they are easy to mix up. They are best understood as answering different questions about a customer relationship: who is this person, who is this company and who really controls it, and is the money moving normally.

A complete program uses several of them together rather than choosing between them. KYB sits within this family:

Term | What it means |

|---|---|

KYC (Know Your Customer) | Verify an individual customer's identity |

KYB (Know Your Business) | Verify a business entity and its beneficial owners |

KYT (Know Your Transaction) | Monitor transactions for suspicious patterns |

KYCC (Know Your Customer's Customer) | Verify the customers your business client serves |

pKYB / pKYC (perpetual) | Continuously re-verify a business or customer on risk triggers |

KYB Regulations by Region

KYB obligations flow from anti-money-laundering law. The Financial Action Task Force (FATF) sets the global baseline, and regions implement it:

Region | Key frameworks | What they require |

|---|---|---|

United States | Bank Secrecy Act, USA PATRIOT Act, FinCEN CDD Rule, Corporate Transparency Act | Identify and verify beneficial owners of legal-entity customers; BOI reporting to FinCEN |

European Union | AML Directives (4/5/6AMLD), new AML Regulation (AMLR) and AMLA | Beneficial ownership registers and harmonized due diligence across the EU |

United Kingdom | Money Laundering Regulations 2017, FCA supervision | Risk-based verification of businesses and their beneficial owners |

Global | FATF Recommendations | Risk-based CDD, beneficial ownership transparency |

KYB Is Not a One-Time Check

A business verified today can change tomorrow: ownership shifts, a director is sanctioned, or adverse media appears. Perpetual KYB (pKYB) moves from periodic reviews to continuous, event-driven monitoring, re-verifying a business when a trigger occurs. Pairing KYB with ongoing transaction monitoring keeps the risk picture current across the whole relationship.

Automating KYB with Qoobiss

Manual KYB is slow: chasing registry documents, mapping ownership by hand, and re-keying data across systems. Qoobiss automates business verification end to end, checking company registries, mapping ownership to surface UBOs, running KYC on directors and owners, and screening the business and its principals against sanctions, PEP, and adverse media sources, all with ongoing monitoring and a clean audit trail.

Frequently Asked Questions

What is KYB?

Are KYC and KYB the same?

What documents are required for KYB?

What is an ultimate beneficial owner (UBO)?

Who needs to perform KYB?

How long does KYB verification take?