Proof of Address: What It Is, What Counts, and How Verification Works

Whether you’re opening a bank account, registering a vehicle, or onboarding customers through a digital platform, there’s a good chance proof of address will come up. It’s one of those requirements that sounds simple until you realize not every document qualifies, rules vary by country, and the line between what’s accepted and what’s rejected isn’t always obvious.

This guide breaks down what proof of address actually means, which proof of address documents pass muster across different contexts, and how both individuals and businesses can navigate the process without unnecessary friction.

What Is Proof of Address?

A proof of address is a document that confirms where a person currently lives. It typically displays the individual’s full legal name alongside a residential address, and must be issued by a recognized authority: a utility provider, financial institution, or government body.

For individuals, proof of address comes up when opening bank accounts, applying for a driver’s license, or enrolling in services that need to confirm your location. For businesses, collecting and verifying proof of address documents is a regulatory obligation under Know Your Customer (KYC) and Anti-Money Laundering (AML) frameworks. Regulators expect organizations to tie each customer to a verifiable physical location, not just a name and an ID photo.

So what is a proof of address in practical terms? It’s worth noting that it is not the same as proof of identity. A passport confirms who you are; a recent utility bill confirms where you live. Most institutions require both, and they typically need to be separate documents.

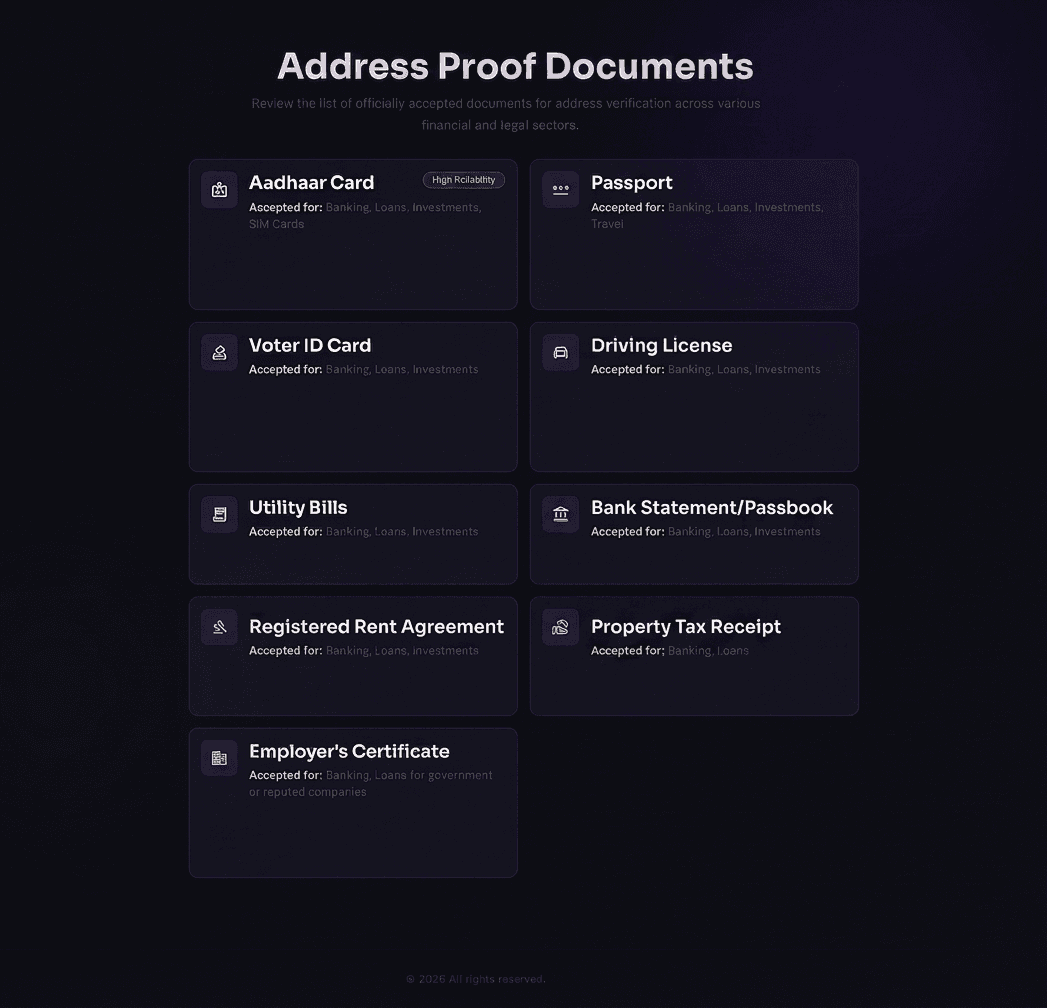

What Counts as Proof of Address? Accepted Documents

What counts as proof of address depends on the institution and jurisdiction, but a few categories are widely recognized. Here are the most commonly accepted proof of address examples:

Document Type | Typical Validity | Notes |

Utility bills (electricity, gas, water, internet) | 3–6 months | Mobile phone bills may not be accepted everywhere |

Bank or credit card statements | 3–6 months | Must show name, address, and recent activity |

Lease or rental agreements | Duration of contract | Some institutions require notarization |

Mortgage statements | 3–12 months | Issued by the lender, tied to a verified property |

Government correspondence | 3–12 months | Tax letters, voter registration, social security notices |

Property tax receipts | Varies | Links the individual to a registered property |

Insurance documents | Varies | Home or auto insurance showing insured address |

Official employer letter | Varies | Must be on company letterhead |

The common thread: documents must be recent, issued by a trusted entity, and clearly display the person’s name and current address. When in doubt, bring more than you think you’ll need; rejection for a technicality is more common than most people expect.

Documents That Don’t Count as Proof of Address

Understanding what can be used as proof of address also means knowing what is considered proof of address and what falls short. The following are frequently rejected:

Handwritten letters or personal correspondence carry no institutional authority. Purchase invoices from online retailers aren’t verified against residential records. Screenshots without official headers, dates, or issuer details are treated as unverifiable. Any document older than three to six months, even from a recognized source, is usually disqualified. Photocopies may also be declined unless they’re certified, depending on the institution’s policy.

The pattern is straightforward: if the document can be easily fabricated or doesn’t originate from a regulated entity, it’s unlikely to pass.

How to Get Proof of Address (Including Without Bills)

For most people, the easiest proof of address is already sitting in their inbox. A recent bank statement, utility bill, or credit card statement downloaded as a PDF and printed will satisfy most requirements. Many banks now allow you to generate an official statement through online banking in minutes, a fast path to how to get proof of address online.

But how to get proof of address without bills? Not everyone has utility accounts in their name, particularly renters, students, or people who’ve recently relocated. Alternatives include a signed rental or lease agreement, a letter from a government agency (tax office, social services, or court), a voter registration confirmation, an employer letter on official company letterhead, or a proof of address letter from a bank confirming your registered address.

If you need a proof of address letter specifically, some banks and building societies will issue one on request; it simply confirms your name and the address they hold on file. This option is particularly useful when you can’t produce a utility bill proof of address or when the document format matters (for instance, if the recipient requires an original letter rather than a printout).

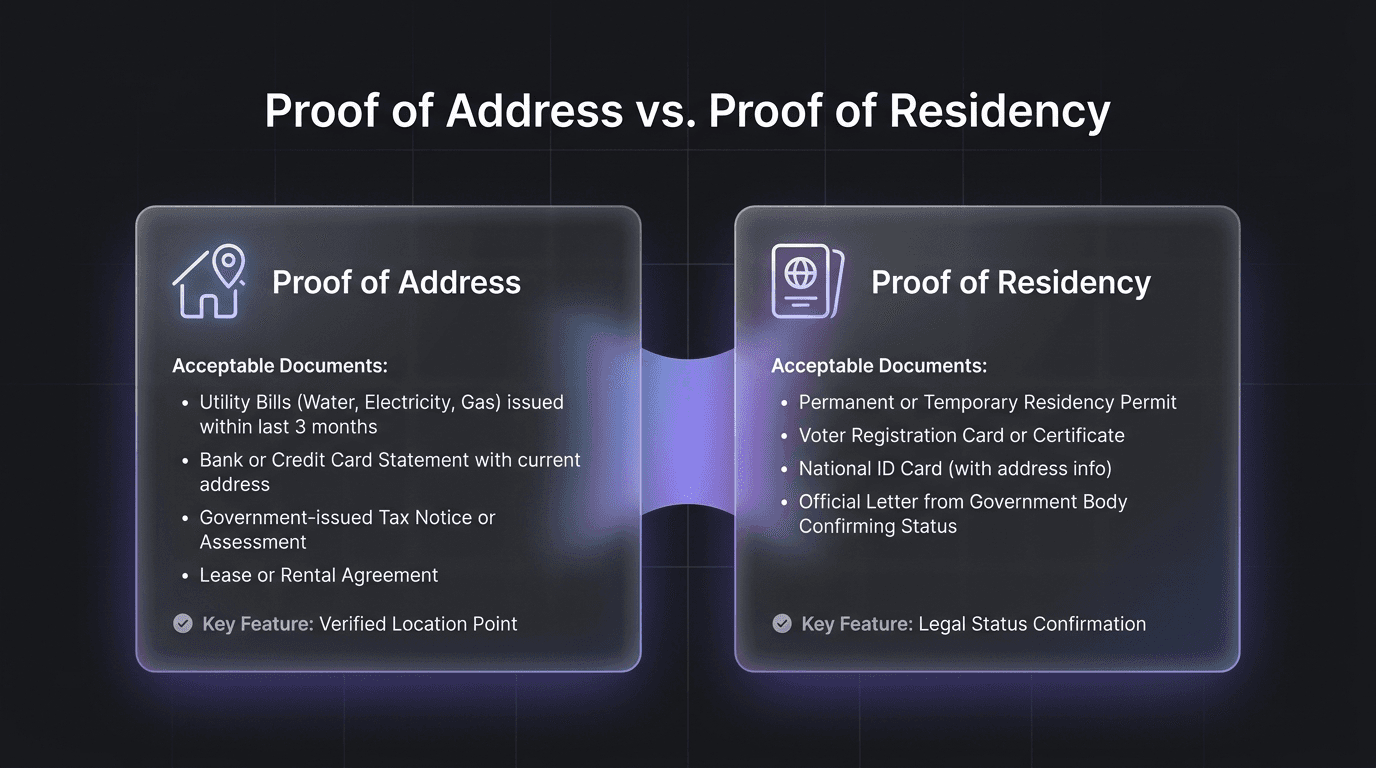

Proof of Address vs. Proof of Residency

These two terms get used interchangeably, but they serve different purposes.

Proof of address confirms where you currently live. It’s typically required for financial services, vehicle registration, and account openings, situations where the institution needs to verify your current location.

Proof of residency, on the other hand, establishes your legal right to live in a country or region. It’s more commonly tied to immigration status, tax residency, or school enrollment. Documents like residence permits, visa stamps, or property deeds fall into this category.

A lease agreement can serve both purposes; it shows where you live and that you have a legal tenancy. But the two aren’t identical, and the wrong one in the wrong context will get sent back.

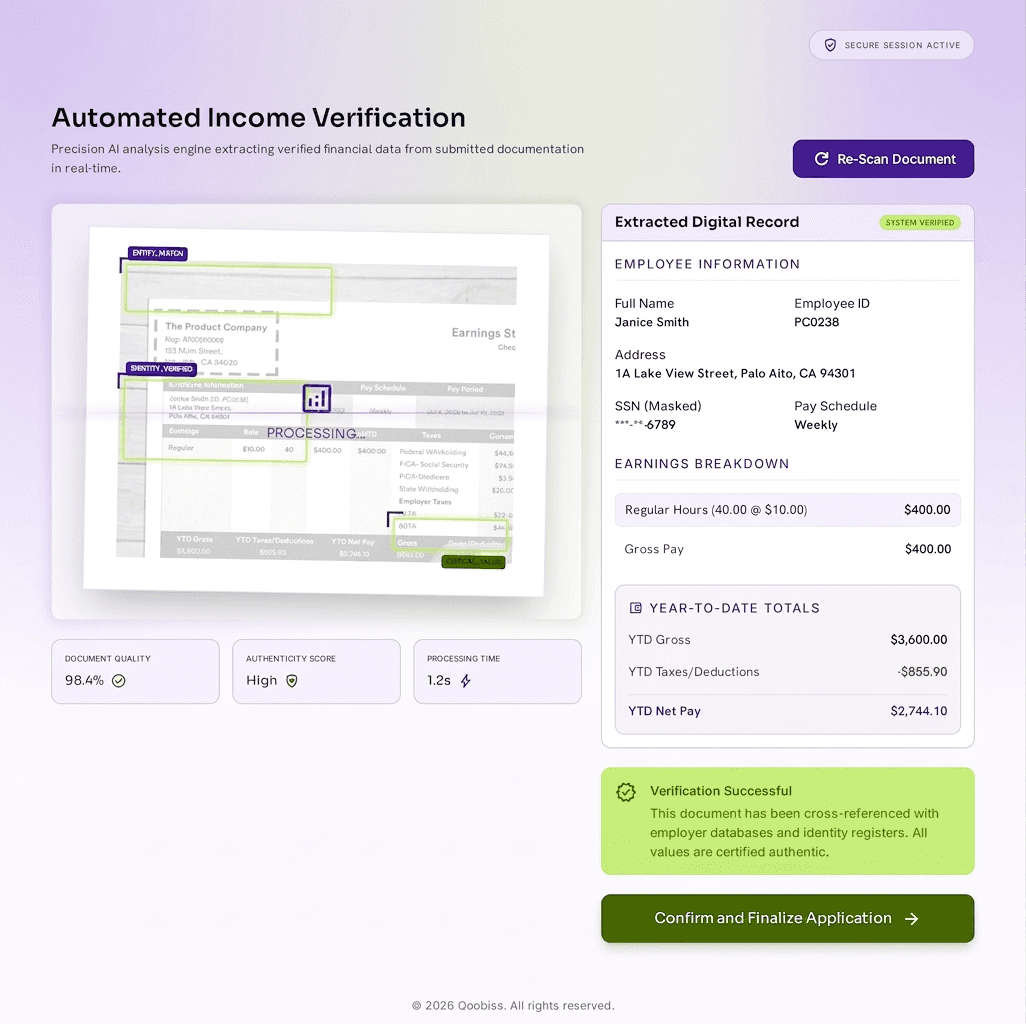

How Proof of Address Verification Works for Businesses

For regulated organizations, proof of address isn’t just about checking a box; it’s an auditable compliance step. The verification process typically follows three stages:

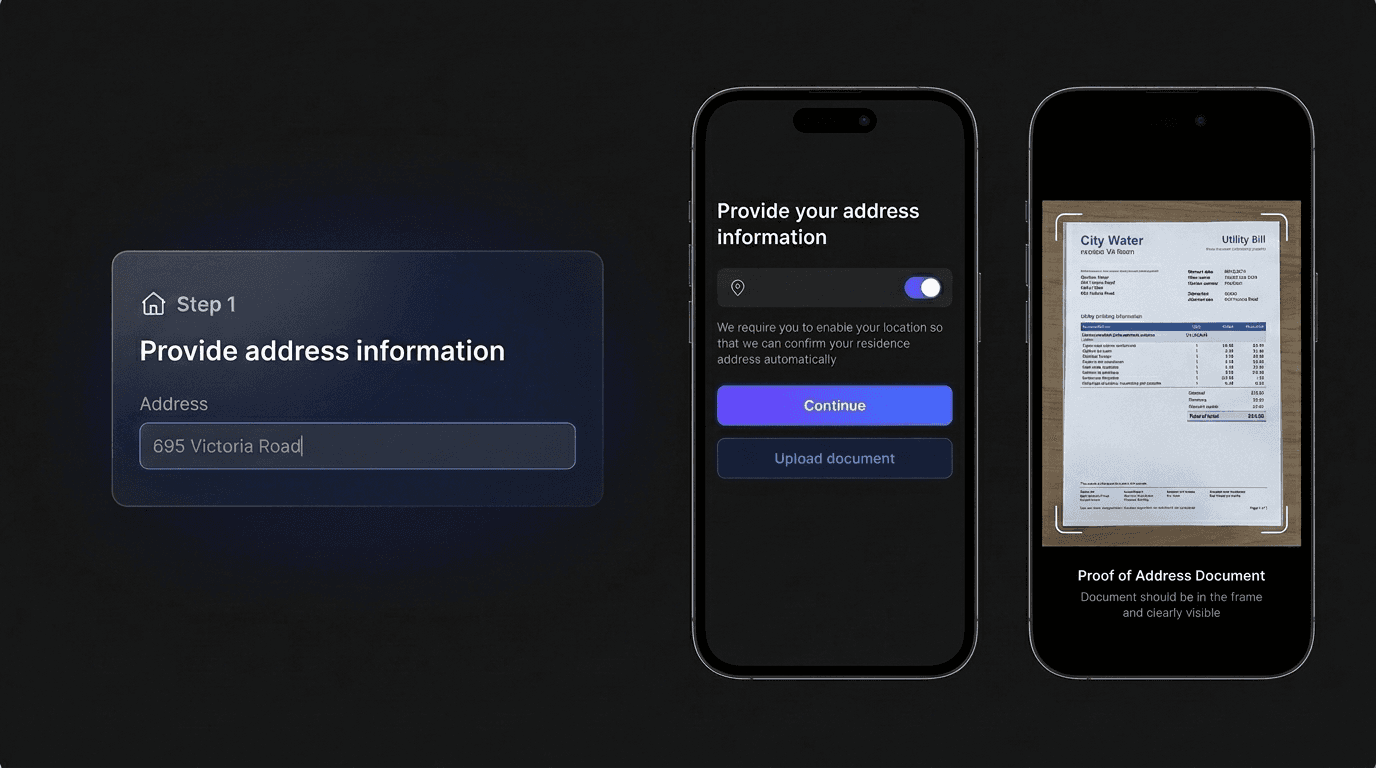

Submission. The customer uploads or presents a document showing their residential address. Clear instructions (accepted formats, validity periods, file types) prevent avoidable rejections.

Validation. The institution checks the document for authenticity and accuracy. Is it recent? Does the name match the customer’s ID? Is the issuer recognized? Automated tools can extract data and flag mismatches or tampering.

Approval or rejection. If standards are met, the address is confirmed and onboarding proceeds. If not, the customer is asked for an alternative, and the rejection reason should be communicated clearly.

For high-volume operations, manual review creates bottlenecks. That’s where automated verification (OCR, metadata analysis, and address database cross-referencing) becomes essential.

Digital vs. Document-Based Proof of Address

Traditional proof of address relies on physical or scanned documents. It works, but paper documents can be forged, scanned copies are easy to manipulate, and review is manual and slow.

Digital proof of address cross-references multiple data points instead: device metadata, geolocation signals, IP analysis, and fraud hotspot databases. Some platforms also verify whether an address is residential rather than commercial or non-existent.

Aspect | Document-Based | Digital Verification |

Speed | Hours to days (manual review) | Seconds to minutes |

Fraud resistance | Moderate (documents can be forged) | Higher (multiple data points cross-checked) |

Scalability | Limited by analyst capacity | Highly scalable |

Customer friction | Higher (document collection, upload) | Lower (fewer manual steps) |

Regulatory acceptance | Universally accepted | Growing, varies by jurisdiction |

The strongest verification programs combine both: using automation for speed while keeping human review for complex or high-risk cases.

Proof of Address Requirements by Industry

Not every sector handles proof of address the same way.

Banking and financial services typically require the most rigorous documentation: a recent utility bill or bank statement within three months, verified against the customer’s ID. For DMV purposes, proof of address DMV applications often have their own accepted list: computer-generated bills, pre-printed pay stubs, first-class mail from a government agency, insurance policies, and motor vehicle registrations are common.

Fintech and digital banking tend to accept a broader range of documents and are more likely to support digital verification methods: e-statements, in-app document uploads, and automated address checks. Some neobanks have reduced proof of address requirements altogether for low-risk accounts.

Crypto exchanges and VASPs face international customer bases where proof of address documents vary widely. Many accept digital bank statements and e-utility bills but apply additional scrutiny for high-risk regions.

Government and DMV offices maintain their own lists; the Colorado DMV, for instance, accepts USPS change-of-address forms and DD214 papers, but rejects junk mail and anything handwritten.

Frequently Asked Questions

Is a bank statement proof of address?

Can I use a utility bill as proof of address?

How recent does proof of address need to be?

Can digital documents be accepted as proof of address?

What if I don’t have any bills in my name?

What’s the difference between proof of address and proof of residency?