Proof of Income: What It Is, What Counts, and How to Show It

Applying for a lease, requesting a loan, or onboarding with a new financial platform almost always triggers the same request: show us what you earn. Proof of income sits at the intersection of personal finance, housing access, and regulatory compliance, and yet the rules around which documents qualify, how recent they need to be, and what to do when you don’t have a traditional pay stub are far from universal.

This guide explains what proof of income actually means, walks through the proof of income documents that institutions accept (and reject), and covers the specific situations such as being self-employment, cash-based work, apartment applications, where standard advice falls short.

What Is Proof of Income?

Proof of income is any official document or record that confirms how much money a person regularly earns or receives. At a minimum, these records identify the payer, the payment period, and the amount, giving landlords, lenders, and institutions a verifiable basis for assessing someone’s ability to meet financial obligations.

For individuals, the concept is straightforward: a landlord needs confidence that you can cover rent, a bank needs to calculate your debt-to-income ratio before approving a mortgage, and a government agency needs to confirm eligibility for assistance programs. For businesses, especially those operating under Know Your Customer (KYC) and Anti-Money Laundering (AML) frameworks. Income verification goes further. It feeds into customer risk profiling, source-of-funds analysis, and ongoing monitoring obligations that regulators expect to see documented and auditable.

What is considered proof of income depends on context. A pay stub may satisfy a property manager, while a mortgage lender will want tax returns spanning multiple years. The thread connecting all of them: the document must originate from a credible source, reflect current earnings, and be difficult to fabricate.

Proof of Income Documents: What Counts

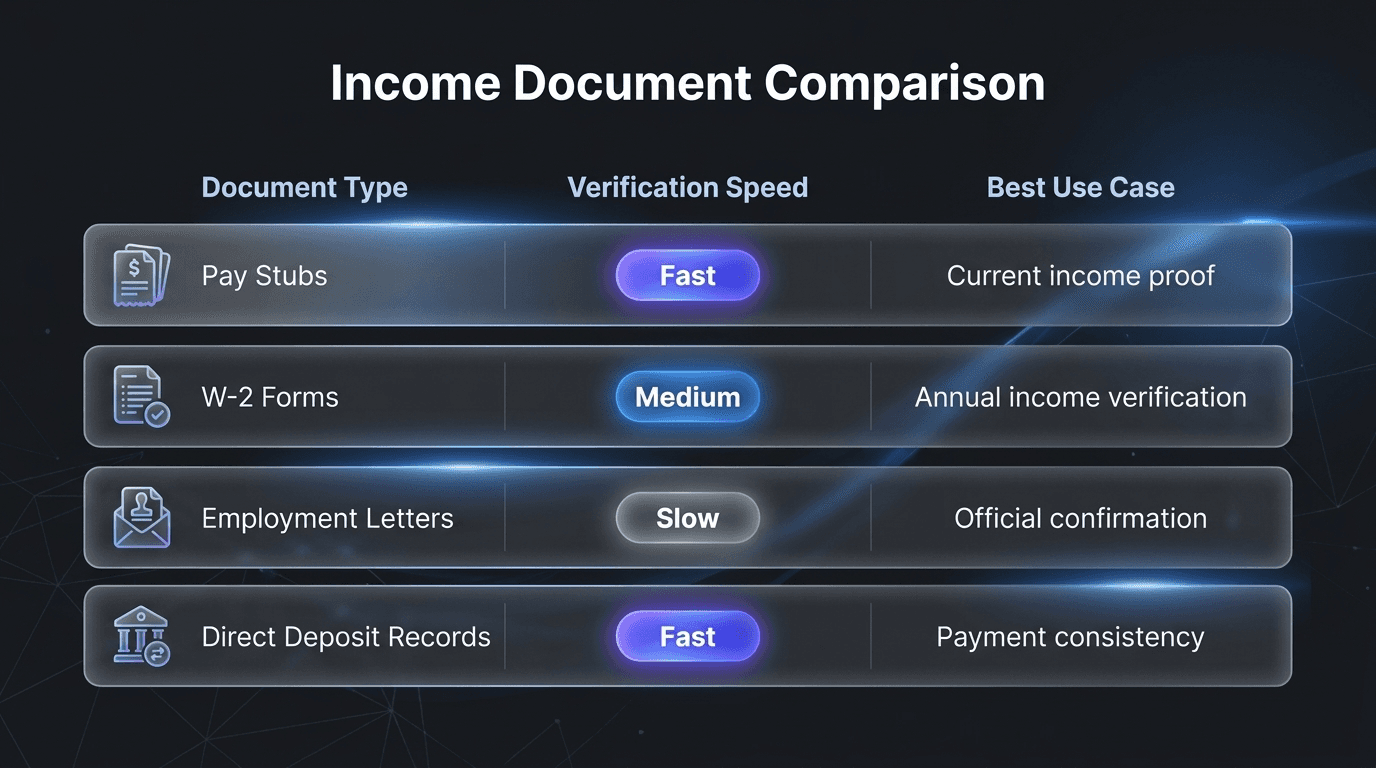

Not every financial record carries the same weight. What counts as proof of income varies by institution, but certain documents are recognized almost universally. Here are the most common proof of income examples:

Document | Who Issues It | Best For | Notes |

Pay stubs | Employer / payroll provider | Salaried and hourly employees | Most landlords ask for 2–3 months of recent stubs |

W-2 forms | Employer (annual) | Year-end income summary | Confirms total annual wages and tax withholdings |

1099 forms | Clients / hiring companies | Freelancers, contractors | Reports non-employee compensation |

Tax returns (Form 1040) | IRS / tax preparer | All earners, especially self-employed | Most comprehensive annual picture |

Bank statements | Financial institution | Supplemental verification | Shows regular deposits; typically 2–3 months required |

Employment verification letter | Employer HR department | New hires, job changers | Confirms title, salary, and employment status |

Profit & loss statement | Business owner / accountant | Self-employed, small business owners | Should cover at least the prior 12 months |

Pension or Social Security statement | Government agency | Retirees, benefit recipients | 1099-R or SSA-1099 confirms benefit amounts |

Court-ordered payments | Family court | Alimony or child support recipients | Details payment schedule and amounts |

Workers’ compensation letter | Insurance provider / agency | Injured workers | Indicates benefit amount and duration |

The common requirement: each document should be recent (typically issued within the last 30 to 90 days), display the recipient’s full name, and come from a source the reviewer can independently verify.

What Doesn’t Count as Proof of Income

Knowing what qualifies is half the picture. Equally important is recognizing what institutions will reject:

Photographs of cash or handwritten tallies carry no institutional credibility. Self-created spreadsheets or personal budgets, no matter how detailed, lack third-party verification.

Screenshots of payment app balances such as: Venmo, PayPal, Zelle, are generally dismissed unless accompanied by formal account statements. Pay stubs older than three months are treated as stale. Cryptocurrency wallet snapshots rarely pass muster without corroborating exchange statements showing fiat conversion.

The underlying principle is consistent: if a document can be easily altered or doesn’t originate from a regulated or recognized entity, it will not satisfy the requirement.

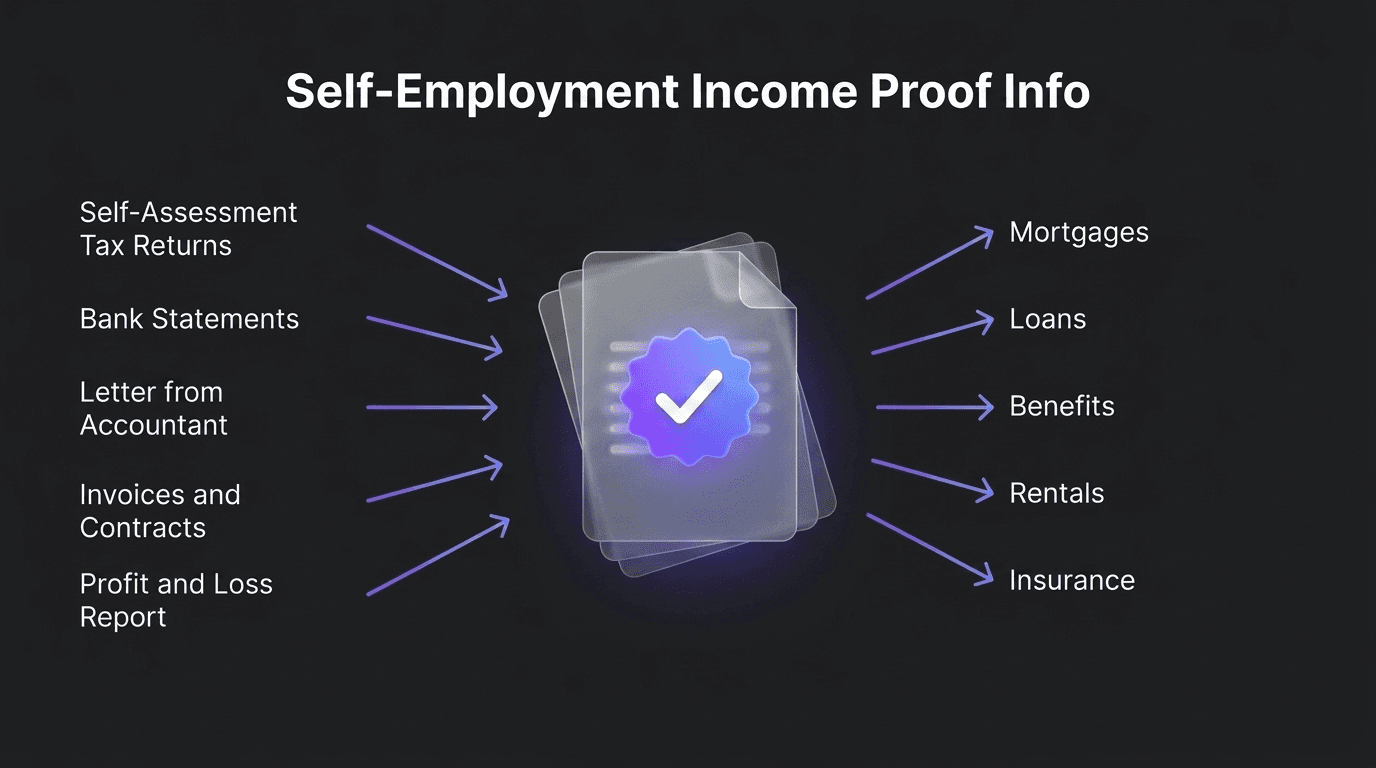

Proof of Income for Self-Employed and Cash Workers

Standard employment produces a tidy paper trail, pay stubs arrive on schedule, W-2s land every January. Self-employment offers no such convenience, which is why proof of income documents for self-employed individuals demand a different approach.

Self-employed workers can typically rely on annual tax returns with Schedule C (reporting business profit or loss), 1099 forms from each client who paid $600 or more during the tax year, bank statements showing regular business deposits over two to three months, a profit and loss statement prepared by the business owner or an accountant, and active contracts or invoices that document ongoing client relationships.

Cash-based workers face the steepest challenge. When income arrives without a digital trail, how to show proof of income if paid in cash becomes a legitimate hurdle. Practical options include maintaining a consistent bookkeeping ledger, even a simple spreadsheet logging each payment with dates, amounts, and client names and then corroborating those entries with bank deposits. A signed letter from a CPA or tax preparer attesting to your reported income carries significant weight. Some landlords and institutions also accept signed statements from clients confirming payment amounts, though these are less universally recognized.

The key for anyone outside traditional employment: start documenting before you need to. Reconstructing months of income history under deadline pressure is far harder than maintaining records in real time.

How to Show Proof of Income for an Apartment

Rental applications are where most people first encounter income verification requirements. Landlords and property managers generally expect applicants to demonstrate earnings of two to three times the monthly rent, a threshold designed to reduce the risk of missed payments.

For traditional employees, the process is usually quick: submit two to three recent pay stubs alongside an employment verification letter. If you’ve recently changed jobs and lack current stubs, a signed offer letter or new-hire letter showing your expected salary serves as a stand-in.

For self-employed renters, expect to provide tax returns from the most recent year, supplemented by current bank statements. Some property managers also ask for a profit and loss statement or active client contracts to gauge income stability.

Co-applicants each need their own documentation. If you’re applying with a partner or roommate, both parties must independently verify their earnings, combined income is assessed, but each person’s contribution needs to be traceable.

If your income comes from non-employment sources: Social Security, disability benefits, alimony, investment dividends, or a pension, official award letters, benefit statements, or brokerage summaries serve as proof of income for apartment applications. The critical point is matching the document to the income type and ensuring it reflects current rather than historical amounts.

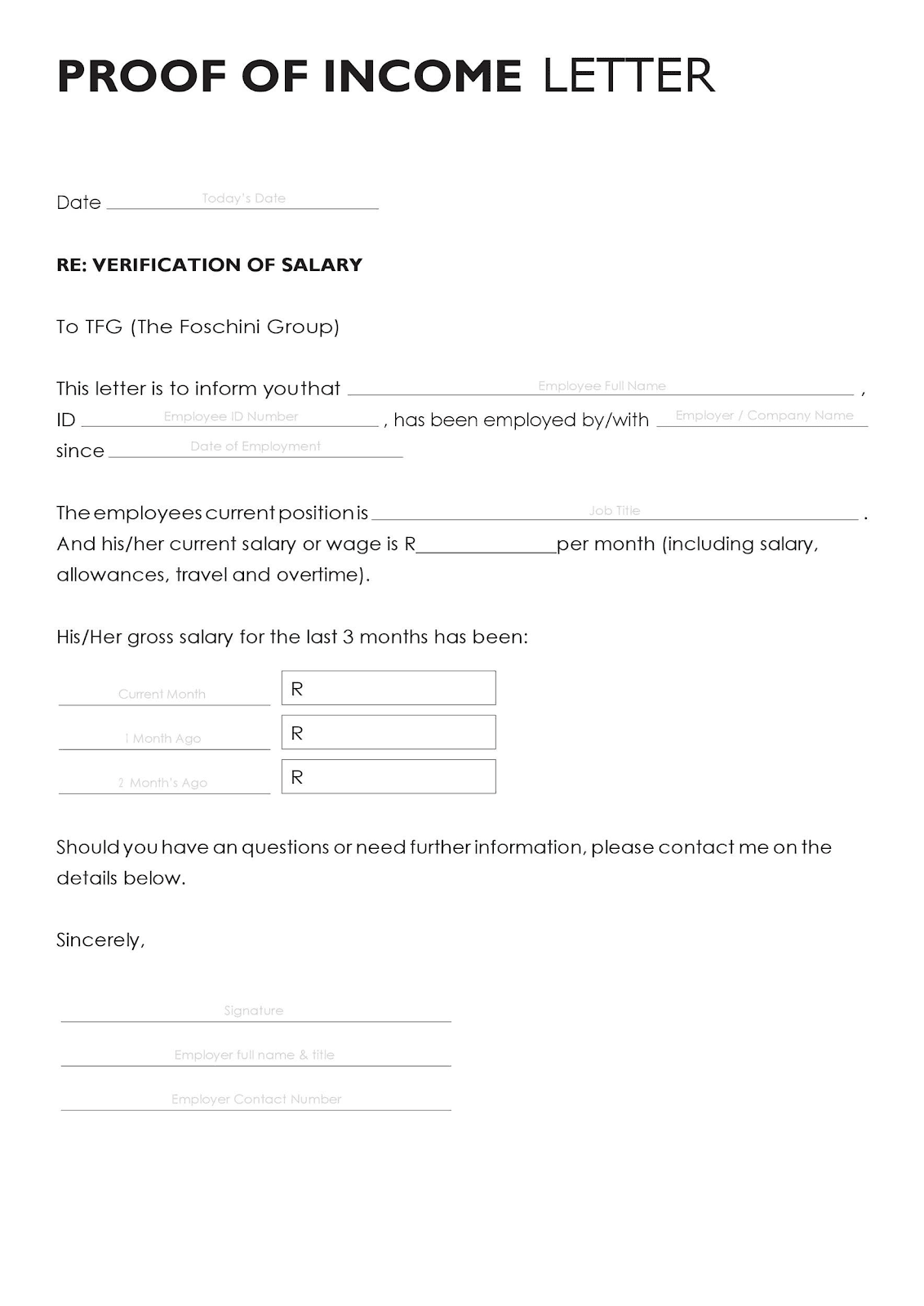

The Proof of Income Letter: What to Include and When to Use One

A proof of income letter is a formal statement usually from an employer, confirming a person’s earnings, job title, and employment status. It serves as a catch-all when standard documents like pay stubs or tax returns are unavailable, insufficient, or need supplementing.

A well-constructed proof of income letter from an employer should include the company name and letterhead, the employee’s full name and job title, their current salary or hourly rate with average weekly hours, the start date of employment, the employer’s contact information for verification, and the signature of an authorized representative (typically an HR manager or direct supervisor).

Self-employed individuals can produce a similar letter by having a CPA or accountant attest to their reported income on professional letterhead, this carries more credibility than a self-authored statement.

When is a letter more useful than a pay stub? If you’ve just started a position and haven’t yet received a paycheck. If your compensation structure involves bonuses, commissions, or irregular payments that stubs don’t fully reflect. Or if the requesting institution specifically asks for written employer confirmation as part of their verification protocol.

Proof of Income Requirements by Context

Different institutions apply different standards. What satisfies an apartment manager may fall short for a mortgage underwriter, and government programs operate under their own frameworks entirely.

Context | Typical Documents Required | Validity Period | Additional Checks |

Rental applications | Pay stubs, employment letter, bank statements | 2–3 months | Income ≥ 2–3x monthly rent |

Mortgages and loans | Tax returns (2 years), W-2s, bank statements, P&L | 2 years + current | Debt-to-income ratio, credit history |

Government assistance | Tax filings, benefit letters, employer attestation | Varies by program | Income thresholds, household size |

Fintech onboarding | Digital bank statements, payroll API data | 1–3 months | Automated data extraction, real-time checks |

For mortgage applications, lenders typically require two full years of tax returns alongside current pay stubs and bank statements, a level of scrutiny that apartment landlords rarely match. Government programs may accept written self-attestation of income in some cases, particularly when applicants face barriers to producing traditional documentation. Fintech platforms increasingly bypass documents altogether, pulling income data directly through payroll integrations and open banking APIs, a shift that is redefining what “proof” looks like.

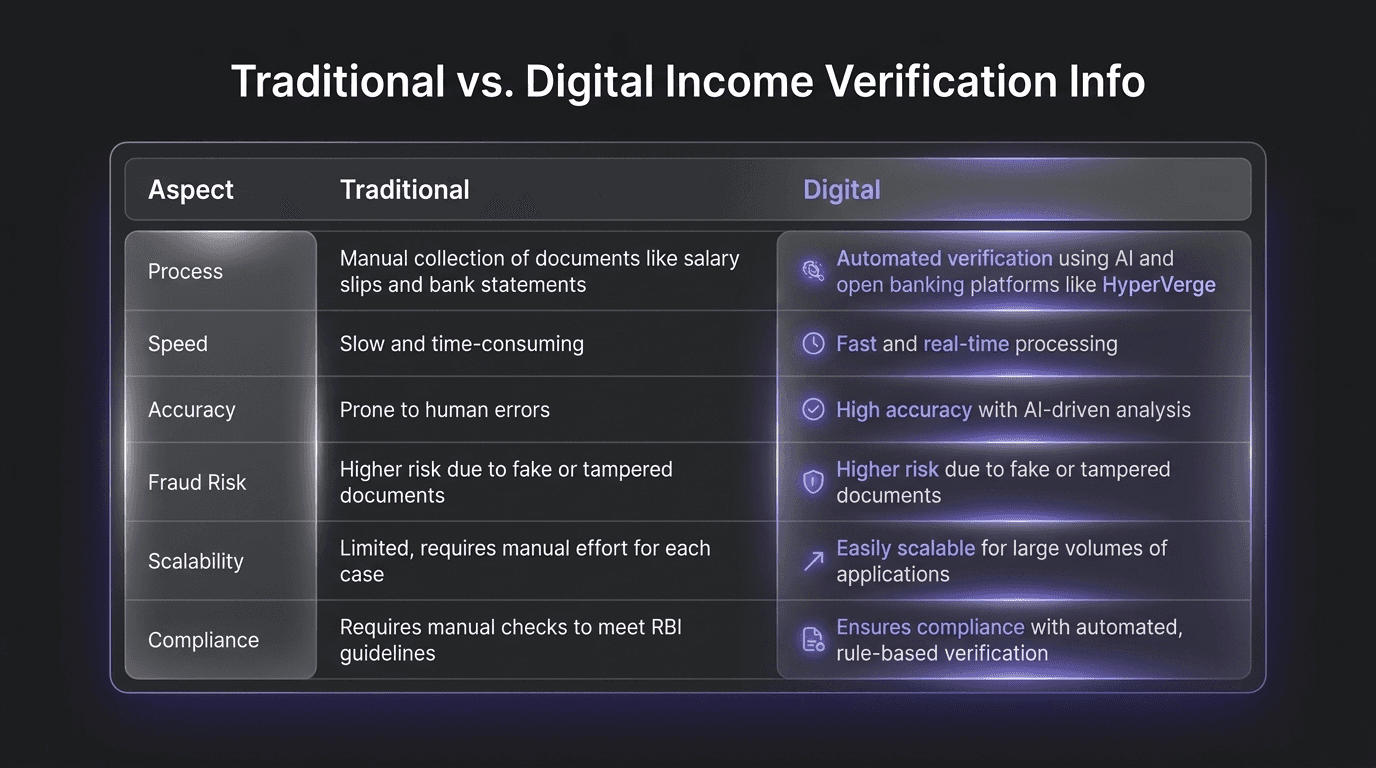

Digital Income Verification vs. Traditional Documents

Collecting pay stubs, scanning bank statements, and waiting for manual review has been the default income verification model for decades. It works, but slowly, and with gaps that document forgers have learned to exploit.

Digital income verification takes a different approach. Instead of relying on static documents, it connects directly to authoritative data sources payroll systems, tax databases, banking APIs, and retrieves earnings information in real time. The result is faster decisions, fewer fabricated records, and a significantly lighter burden on the person being verified.

Aspect | Document-Based | Digital Verification |

Speed | Hours to days (manual review) | Seconds to minutes |

Fraud resistance | Moderate (documents can be forged or edited) | Higher (data pulled from source systems) |

Scalability | Limited by analyst capacity | Highly scalable across thousands of verifications |

Customer friction | Higher (locate, scan, upload documents) | Lower (authorize a connection, data flows automatically) |

Regulatory acceptance | Universally accepted | Growing rapidly, varies by jurisdiction |

The most effective verification programs layer both methods, using digital checks as the primary path for speed and accuracy, with document-based review available for edge cases or jurisdictions where electronic verification hasn’t yet achieved full regulatory acceptance.

Frequently Asked Questions

Are bank statements proof of income?

How to show proof of income without pay stubs?

How to show proof of income if paid in cash?

What is considered proof of income for self-employed individuals?

How recent does proof of income need to be?

Can digital income verification replace paper documents entirely?